General Crypto

April 9, 2026

Congress Has Been Beating the Stock Market by 112% and the Fine Is $200

Global Flash PMIs will be released next week on Tuesday, March 24. S&P Global will publish preliminary readings for manufacturing, services, and composite activity across the US, Eurozone, and the UK. Markets expect these early indicators to provide fresh clues about economic momentum in the first quarter, amid tensions in the Middle East.

The key points are the balance between resilient services sectors and any manufacturing recovery signals which often influence broader sentiment. Stronger figures have historically lifted risk assets such as stocks and cryptocurrencies by signaling expansion without forcing quick policy changes.

Also Read: Oil Inventories & EIA Report: U.S. Supply Outlook Amid Escalating Iran Tensions

S&P Global will release the Global Flash PMIs on Tuesday, March 24, 2026. The schedule starts with Eurozone figures, followed by UK data, and then US manufacturing PMI data plus services PMI outlook. These preliminary “flash” estimates arrive roughly one week ahead of the final monthly numbers. They give markets the first reliable snapshot of business activity trends across major economies.

Traders prioritize the composite index most. It blends manufacturing PMI data and services PMI outlook into one headline figure that best reflects overall private-sector health. The US composite often carries the heaviest weight for global sentiment.

Eurozone and UK readings help calibrate regional divergences. Any surprise deviation from consensus forecasts can quickly shift rate cut expectations. Results can also trigger immediate stock market reactions. The final (not flash) PMI readings follow later in the cycle. It is worth noting that the European Central Bank (ECB) is expected to hold a key decision meeting in late April.

S&P Global publishes the complete and revised Global Flash PMIs data on April 1, 2026, for the March period across all covered economies. Until then, the flash version remains the dominant driver.

Also Read: MicroStrategy Bitcoin Purchase: Why Monday Matters for Investors

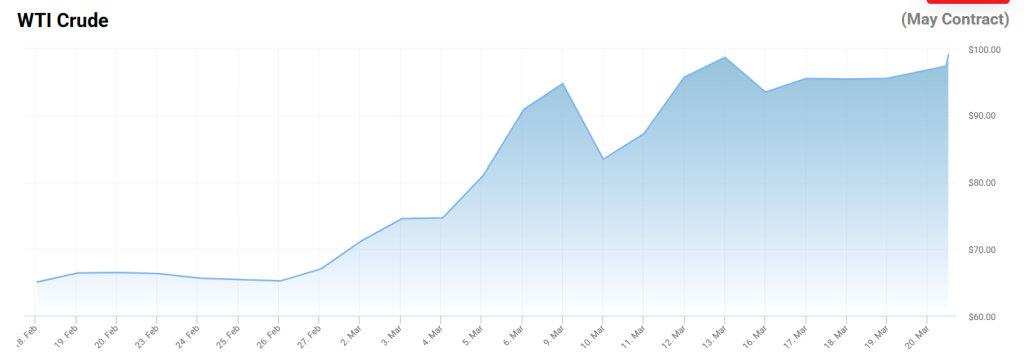

The US-Iran conflict, now entering its third week, has escalated with targeted strikes on energy infrastructure and renewed threats around the Strait of Hormuz. Oil prices have surged above $105 per barrel, pushing input costs higher for manufacturers worldwide. These Global Flash PMIs mark the first major survey wave since the conflict intensified in early March. This captures initial business responses to elevated energy prices and supply-chain pressures.

Manufacturing PMI data will therefore draw extra attention. Firms report on cost pass-through, order backlogs, and production adjustments amid the new geopolitical reality. A resilient reading could signal that manufacturers are absorbing shocks effectively and maintaining output, supporting broader growth views.

Meanwhile, the services PMI outlook remains less directly exposed to oil volatility, offering a counterbalance if it holds firm. Strong overall prints would temper inflation fears from the conflict and keep rate cut expectations anchored, while any weakness might accelerate stock market reaction toward defensive sectors. Traders see this as an opportunity to gauge real-economy resilience under pressure.

Also Read: Winklevoss Twins Cut 30% of Gemini Staff After $585M Loss and Three Exits