Markets

July 15, 2026

Is The Gulf Rebuilding Its Oil Network to Bypass the Strait of Hormuz?

PayPal stock has spent much of the past year trading under the weight of cautious analyst sentiment. But a surprise bid from Stripe and Advent has suddenly changed the narrative. The reported offer values the payments giant well above where both the market and many analysts see it today. This gap is what has investors paying attention, as the proposed PayPal acquisition raises fresh questions about the company’s long-term value.

Also Read: One Wall Street Bull Sees S&P At 8,000 While Others Warn Of the AI Bubble Burst

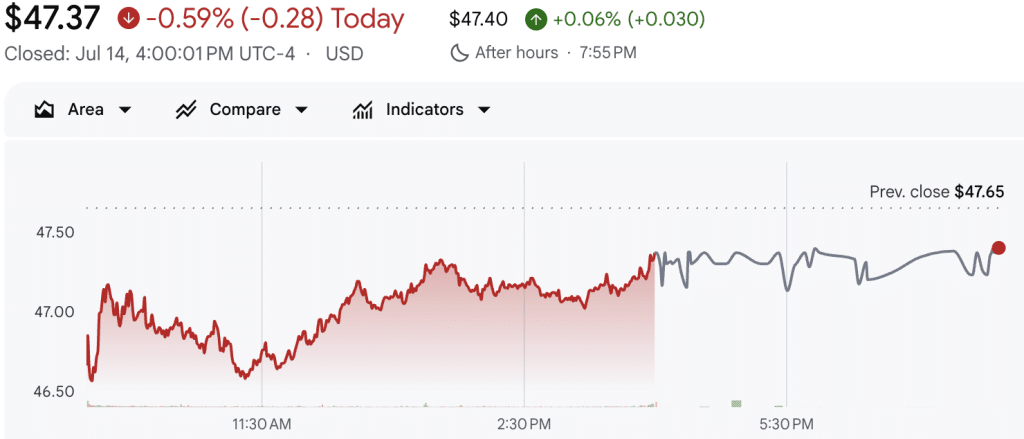

According to reports, Stripe and private equity firm Advent International have offered $60.50 per share to acquire PayPal in a deal worth more than $53 billion. The proposal, submitted earlier this month, is backed by roughly $50 billion in committed financing from banks. It represents a 28% premium to PayPal’s latest closing price of $47.37.

The offer follows an initial approach made in April, with sources noting that Stripe and Advent are still waiting for PayPal’s response. Under the proposal, the two companies would jointly own PayPal through equal stakes rather than splitting up the business. While discussions remain ongoing, there is no certainty that the talks will lead to a transaction.

The structure of the proposed deal suggests the buyers are betting on PayPal as a long-term payments platform instead of pursuing a breakup or asset sale. This comes at a time when consolidation is picking up across the payments industry. Companies seem to be seeking greater scale and exposure to faster-growing areas such as cross-border transactions, digital wallets, and business-to-business payments.

The timing stands out here. Once valued at nearly $360 billion during the pandemic, PayPal has spent the last several years trying to regain investor confidence. This is after slowing growth and rising competition from Apple Pay, Google Pay, and newer fintech firms. The company’s market capitalization briefly fell to around $36 billion this year. It lost more than 40% of its value over the past 12 months. The proposed deal could mark a turning point for PayPal stock.

Since taking over in March, CEO Enrique Lores has launched a restructuring aimed at simplifying the business and boosting growth. In April, PayPal reorganized its operations into three core divisions covering checkout, Venmo and consumer financial services, and payments and crypto. They also reshuffled parts of its leadership team.

Also Read: SpaceX Share Price Slides to a Record Low as IPO Euphoria Fades

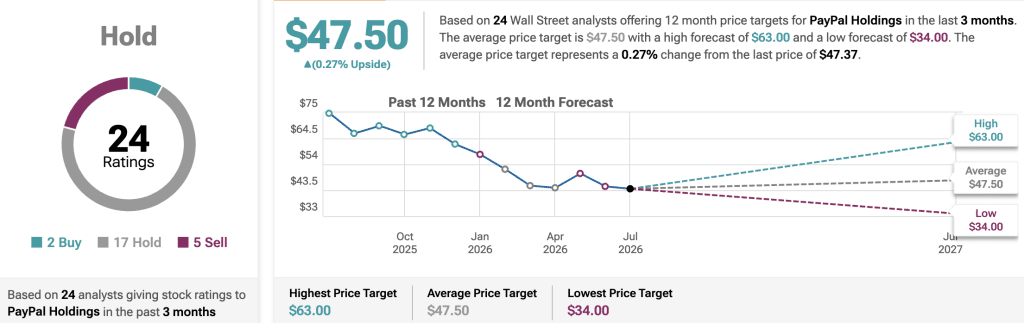

The reported Stripe-PayPal proposal also stands in contrast to Wall Street’s current expectations. According to TipRanks, 24 analysts covering the company have assigned PayPal stock an average 12-month price target of $47.50. This is almost identical to its latest market price, alongside a consensus Hold rating. Only two analysts rate the shares a Buy, while 17 recommend Hold and five maintain Sell ratings. The highest published price target stands at $63, with the lowest at $34.

For potential buyers, however, PayPal appears to be worth considerably more. A $60.50-per-share offer places the company near the upper end of analysts’ expectations. It suggests strategic investors see value beyond the market’s current assessment. Whether the PayPal acquisition moves ahead or not, the reported bid has already shifted the conversation surrounding PYPL stock from short-term execution to long-term strategic value.

Also Read: Samsung Stock Rises Despite ADR Denial as Anthropic AI Chip Deal Boosts Optimism

Written by Sahana Kiran

Sahana Kiran has been covering financial markets since 2019, with a focus on cryptocurrencies, fintech, and the geopolitical events shaping them. She previously reported for AmbCrypto and Watcher Guru, and now writes for BlockNow.