General Crypto

June 28, 2026

Bitmine Q3 Reality Check: BMNR Earnings Squeezed by Bitcoin Mining Pressures

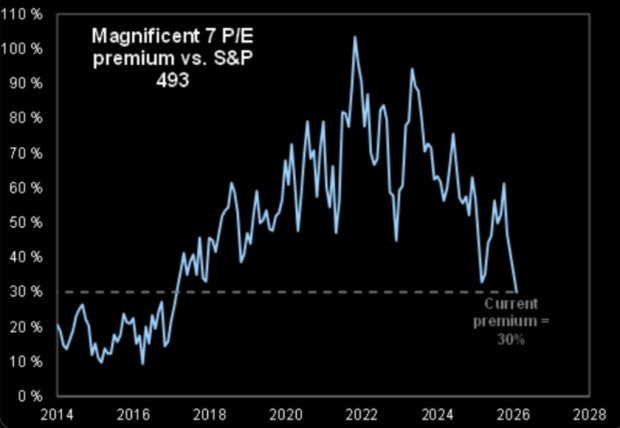

Mag 7 GARP stocks are changing how Wall Street thinks about Big Tech in 2026. With AI capex bills climbing sharply and free cash flow pressure showing up in quarterly results, the Magnificent Seven’s P/E premium over the S&P 493 has collapsed to just 30%, the lowest in a decade, and that reset is turning these names into a real growth at a reasonable price conversation. The Roundhill Magnificent Seven ETF (MAGS) is down nearly 6% year to date, Microsoft has shed nearly 18%, Tesla and Amazon have each dropped more than 8%, and Nvidia is up just 1% at the time of writing.

Also Read: US Senate Probes Binance Over Iran, Russia Flows and WLFI Trump Ties

The Nifty 50 comparison keeps coming up on Wall Street, referring to a group of stocks that commanded 40x P/E multiples in the early 1970s before suffering drawdowns of 50% or more during the 1973 to 1975 recession. The Mag 7 GARP stocks thesis runs on a different set of numbers. Right now, the average forward P/E for the Mag 7 sits at roughly 28x, against 23.5x for the S&P 500, the narrowest premium gap in ten years, per Zacks Investment Research. Big Tech valuations have come in hard, and earnings are not helping either.

Barclays analyst Venu Krishna stated:

“Big Tech EPS surprise is tracking at +5.3%, below the LT median of +7.2%, and unlike last quarter, there were no large one-time charges weighing down the group’s overall beat. EPS deceleration is contributing to multiple compression.”

Alphabet, Amazon, Meta, and Microsoft plan to spend nearly $700 billion combined on AI capex this year, up roughly 60% from 2025. Their combined free cash flow dropped from $237 billion in 2024 to $200 billion last year. Microsoft now expects roughly flat free cash flow for the first time in years, and Amazon posted an $11.2 billion drop in Q4 free cash flow alone. That kind of free cash flow pressure also explains a lot of the move in Big Tech valuations this year, and it is also what makes the growth at a reasonable price argument more credible right now than it has been in a while.

Hightower Advisors Chief Investment Strategist Stephanie Link mentioned:

“The catalyst for the initial selling was some of them having negative free cash flow, and some of them just having flat year-over-year cash flow, as opposed to both that we have been seeing over the last decade with these companies.”

Melius Research analyst Ben Reitzes also wrote in a note to clients:

“We wouldn’t be surprised if Broadcom generated more free cash flow than MSFT this year when it’s all said and done. The cash goes right from one place (the hyperscalers) and into another (NVDA, Broadcom and other infrastructure names) … Investors are voting with their feet so far this year since nobody can figure out hyperscaler free cash flow in the 2030s for their mental DCF model.”

Also Read: Coinbase Opens Stock and ETF Trading to All US Users With Yahoo Finance

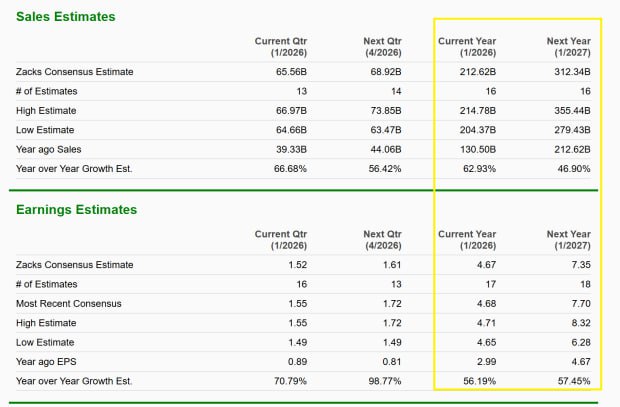

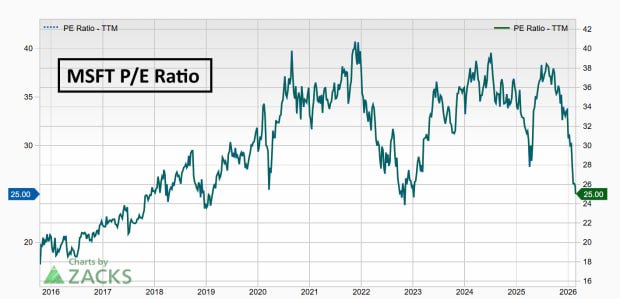

Not every Mag 7 GARP stock looks the same right now. NVIDIA, at a $4.6 trillion market cap, still has Zacks Consensus Estimates pointing to roughly 50% top-and-bottom-line growth over the next two years, a textbook growth at a reasonable price setup. Microsoft’s P/E sits at its lowest since late 2022, right before the ChatGPT rally pushed it sharply higher, and analysts still project double-digit growth despite the AI capex overhang. Numbers like these make the bull case for Mag 7 GARP stocks hard to fully dismiss.

Bryn Talkington, founder and managing partner of Requisite Capital Management, was clear about the fact that:

“When you actually look at earnings and margins, squarely, all of the earnings and margins still come from tech … The market does not like the capex spend and until there’s a clear line of sight for what these companies are solving for, the Microsofts, the Amazons will continue to be under pressure.”

Citi moved to reflect this uncertainty, downgrading technology to neutral and shifting half of its overweight tech holdings into cyclicals. The rotation also tells you a lot about how much Big Tech valuations have worn on growth-at-any-price investors. Free cash flow pressure and AI capex spending cycles are real headwinds, and Mag 7 GARP stocks are sitting right in the middle of that tension.

GDS Wealth Management CIO Glen Smith stated:

“Mag 7 stocks are struggling this year simply because these stocks are exhausted. These are incredible companies and incredible stocks, but at some point, a breather is needed. So much of the AI-related boost has already been priced in.”

Also Read: Gold Surpasses US Dollar as Top Reserve Asset Amid China’s $369.6B Surge

With AI capex cycles still running and Big Tech valuations reset to decade-low premiums, Mag 7 GARP stocks now sit in an unusual spot. The growth at a reasonable price argument has not looked this credible in years, and whether it plays out depends almost entirely on what those massive AI bets actually deliver.

Written by Vladimir Popescu

Vladimir Popescu leads editorial coverage at BlockNow, with over 8 years in financial and tech journalism. He previously held editorial leadership roles at Watcher Guru and Windows Report, and has been cited by Forbes for his crypto market coverage.