Markets

June 25, 2026

Anthropic Accuses Alibaba of Largest AI Model Extraction Campaign as US-China AI Race Heats Up

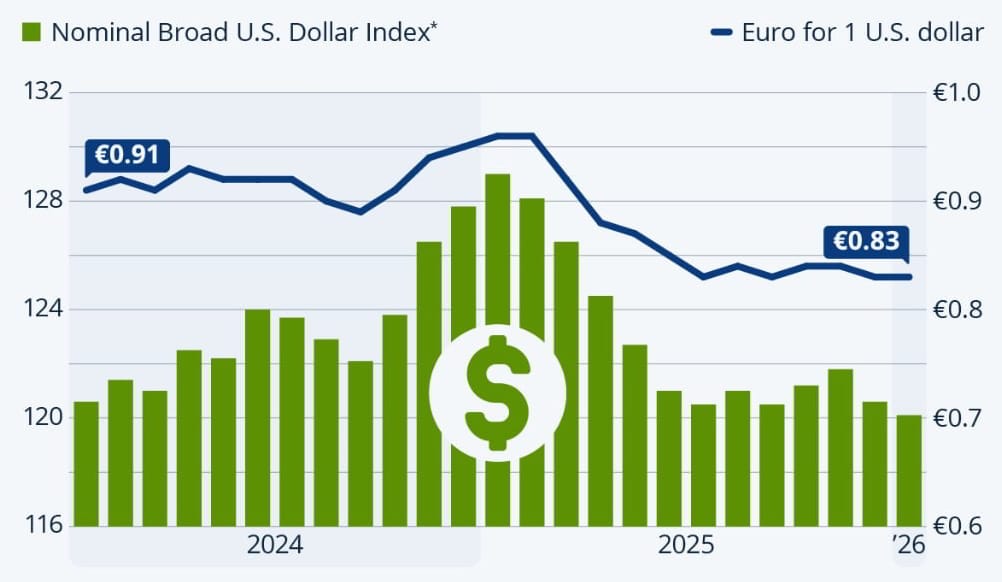

Dollar dominance being questioned is almost a fixture of the financial calendar at this point, but this month’s version has more substance to it than most. The US Dollar Index sits at 98.39 as of April 22, 2026, well below its 52-week high of 101.98, and Deutsche Bank and Franklin Templeton published competing notes with views about as far apart as they get. Westpac’s US dollar weakening forecast is also out, and it points to meaningful further losses for the greenback through 2026.

Also Read: Global Financial Strain Pushes BRICS And G20 Into Action

Things got going on March 24, when Deutsche Bank FX managing director Mallika Sachdeva published a note pointing to the Iran war, which started on Feb. 28, as a potential turning point for the dollar. In her view, the conflict could go down as a key catalyst for “erosion in petrodollar dominance, and the beginnings of the petroyuan.” Gulf countries pricing crude in alternative currencies would, in that scenario, signal a real shift in how global trade works.

Franklin Templeton’s US dollar team had a different view. Their note, published on April 14, called the Deutsche analysis “remarkably simplistic” and argued that Sachdeva misread the relationship between US security guarantees and oil pricing. That exchange captures the dollar dominance questioned argument in 2026 fairly well. Fixed income CIO Sonal Desai stated:

“Oil is not priced in US dollars simply because the United States has long acted as the world’s policeman. Oil exporters have a strong self-interest in getting paid in USD, because of what dollars represent: access to the deepest, most liquid capital markets in the world, backed by an institutional and legal framework that protects property rights and enforces contracts, supported by a strong, dynamic, and innovative economy.”

Also Read: The UAE Just Threatened to Price Oil in Yuan Unless America Bails It Out

With dollar dominance questioned across multiple fronts, the numbers tell part of the story. Dollar reserves fell from over 70% in 1999 to just above 50% today, and the dollar index dropped nearly 10% through 2025, its worst run in over 50 years.

Brown Brothers Harriman’s Elias Haddad, global head of markets strategy, still sees no replacement anywhere on the horizon. Haddad told CNBC:

“There is no alternative. All other currencies are nowhere near an environment to replace the dollar.”

On China’s renminbi specifically, Haddad added:

“There’s no way China is going to get to 50% anytime soon, especially with their capital markets closed. It’s the same for the Eurozone.”

Dollar dominance is questioned, sure. But Haddad’s point stands: no other currency has the infrastructure to back it up.

There is a reason dollar dominance is questioned. Westpac’s US dollar weakening forecast puts the DXY on a path toward the mid-90s by late 2026, with euro, sterling, yen, and some emerging market currencies set to gain. The dollar dominance debate, in Westpac’s read, has a real structural basis right now, and the bank sees the balance of risks leaning firmly to the downside.

Also Read: Iran Shut Hormuz Again and Trump Just Gave Tehran a Wednesday Deadline

Even so, Franklin Templeton’s US dollar note drew a clear line between short-term softness and actual structural collapse. Building credible reserve infrastructure, which Desai described as “deep markets, rule of law, full convertibility, a track record of macro stability,” takes decades, not years. Desai also stated:

“Some dollar softness is perfectly consistent with global reserve currency status. Unlike the renminbi, the dollar is a freely floating currency. It floats — up and down.”

The weakening trend is real, and the US dollar future looks more uncertain than it did a few years back. Deutsche Bank sees a structural decline already underway, while Franklin Templeton and BBH land in a different place entirely. Both institutions agree the dollar has taken hits, from fading fiscal credibility to Fed pressure to the Iran war, but neither sees a single currency with the markets, the legal framework, or the track record to actually take its place.

Written by Vladimir Popescu

Vladimir Popescu leads editorial coverage at BlockNow, with over 8 years in financial and tech journalism. He previously held editorial leadership roles at Watcher Guru and Windows Report, and has been cited by Forbes for his crypto market coverage.