Business

August 6, 2026

Wall Street Targeted by Hackers as Meta Discloses AI Cybersecurity Incident

Key Takeaways

Accenture plc releases third-quarter fiscal 2026 results on June 18. Accenture Earnings will show whether AI revenue growth continues to offset softer federal spending and cautious enterprise budgets. The company reports revenue, new bookings, and updated guidance amid shifting consulting demand. Analysts watch margins and segment performance closely. The outcome highlights how Accenture balances strong AI momentum with broader economic pressures in technology services.

Also Read: Inside the Bitcoin Drop: How MSTR Sale Sparked a Global Crypto Rotation

Accenture Earnings arrive on June 18 with fresh detail on AI performance. Observers focus on the share of revenue tied to generative AI and advanced automation services. Executives plan to disclose specific AI-related bookings achieved during the quarter. These numbers indicate early traction in high-value enterprise work.

AI revenue growth stands out as the clearest sign of strategic progress. The company also reports how consulting demand holds up across financial services, health, and communications. Slower federal spending creates pockets of softness that management must address. Analysts track the contribution from AI solutions within overall new bookings.

They compare results against the prior revenue forecast. Strong execution here reinforces Accenture’s leadership in digital reinvention. The figures together paint a clear picture of how the firm converts technology interest into sustained business gains.

Also Read: IPO Bubble Alert: Tech and AI Valuations Hit Peak Risk Levels

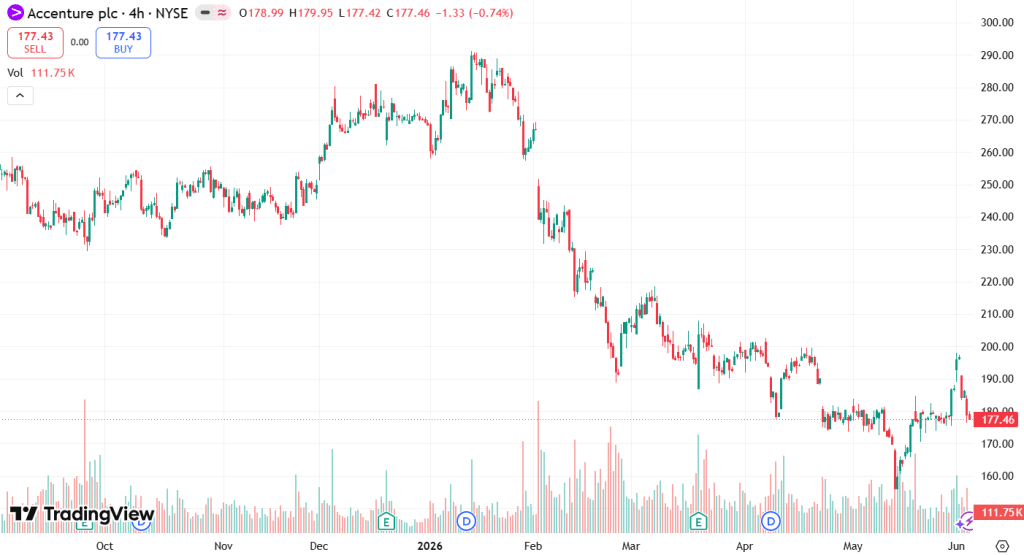

Accenture Earnings on June 18 could clarify whether AI revenue growth delivers a decisive premium capable of reversing recent share price pressure. Over the last several months, ACN stock has traded sharply lower from 2025 peaks near $380, falling more than 40 percent amid broader sector rotation and concerns over spending patterns.

Shares touched lows around $156 before a partial recovery into the mid-$180s in recent weeks.Strong AI revenue growth stands as the potential catalyst for renewed momentum. Management highlighted accelerating bookings from generative AI and automation platforms in prior updates. This performance could lift the revenue forecast if conversion rates improve and enterprise commitments expand.

Consulting demand remains solid in commercial segments even as federal spending stays restrained. A convincing beat combined with raised guidance may convince investors that the AI premium justifies higher valuations. Blocknow recently reported on Marvell Q1 earnings and the importance of AI cloud centers for valuations. Success here would mark a meaningful breakout from the current trading range and restore confidence in Accenture’s premium positioning.

Also Read: Panic Selling Triggers 50% Zcash Crash as Network Bug Exposed

Written by Carlos Terenzi

Carlos Terenzi is a financial analyst with over 10 years of experience in crypto, finance, and international relations, focusing on Bitcoin, monetary policy, and precious metals.