Stocks

August 1, 2026

SanDisk Q4 Earnings Near After 57% Drop And Sudden Share Bounce

Apple (AAPL) stock has spent the past few weeks rewriting its own record book. Its latest rally suggests investors are buying into something bigger than momentum. As much of Big Tech pours billions into artificial intelligence infrastructure, Apple has mostly stayed on its own path. This approach, paired with resilient earnings and a growing services business, is beginning to reshape how Wall Street values the company. Citi’s latest upgrade only added fuel to that narrative.

Also Read: Gold Eyes $10K as Silver Breakout Adds to Bullish Precious Metals Outlook

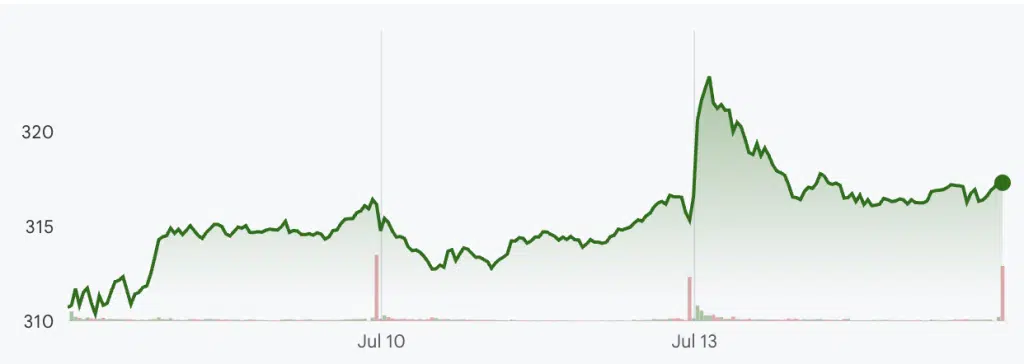

AAPL stock climbed to a fresh all-time high. It managed to rally, which has seen the stock gain about 17% over the last 10 trading sessions while adding close to $688 billion to the company’s market capitalization. The move has pushed Apple’s value toward $4.7 trillion. This highlighted its position as one of the world’s most valuable listed companies.

Unlike rivals including Microsoft, Meta, Amazon, and Alphabet, Apple has avoided an aggressive AI spending race. While those companies continue investing heavily in data centers and AI infrastructure, Apple’s more measured approach has helped preserve its free cash flow and operating margins.

This hasn’t come at the expense of growth. Apple’s latest quarterly results showed Services revenue reached another record. This was supported by continued strength across subscriptions and digital offerings. The iPhone business has also remained more resilient than many analysts expected despite concerns over slowing consumer demand.

Also Read: Trump Urges Senate to Pass CLARITY Act as US Government Moves $288M in Bitcoin & Ethereum

Wall Street has become divided over Apple stock. Citi raised its Apple price target from $315 to $365 while maintaining a Buy rating. They cited improving earnings expectations, continued strength in the Services business, healthy margins, and confidence in Apple’s long-term ecosystem.

KeyBanc, however, moved in the opposite direction. The firm downgraded Apple to Underweight from Sector Weight and assigned a $250 price target. They argued that iPhone shipments could slow as higher prices, weaker US upgrade cycles, and changes to carrier subsidy programs weigh on demand.

KeyBanc also warned that growth across Apple’s Mac, iPad, Wearables, and Services businesses could soften in 2027. They added that the company’s current valuation leaves little room for operational missteps.

For investors, the opposing calls point to a much bigger debate. Bulls see Apple’s disciplined AI spending, resilient cash generation, and ecosystem as reasons the rally can continue. Bears believe much of that optimism is already reflected in the share price after its rapid climb to record highs.

Also Read: US Debt Hits $39.4 Trillion as Interest Payments Soar and 30-Year Treasury Yield Tops 5%

Written by Sahana Kiran

Sahana Kiran has been covering financial markets since 2019, with a focus on cryptocurrencies, fintech, and the geopolitical events shaping them. She previously reported for AmbCrypto and Watcher Guru, and now writes for BlockNow.