Bitcoin

June 16, 2026

BlackRock’s First Bitcoin Yield ETF Launches Today as XRP Whales Control 74.1% of Supply

Key Takeaways

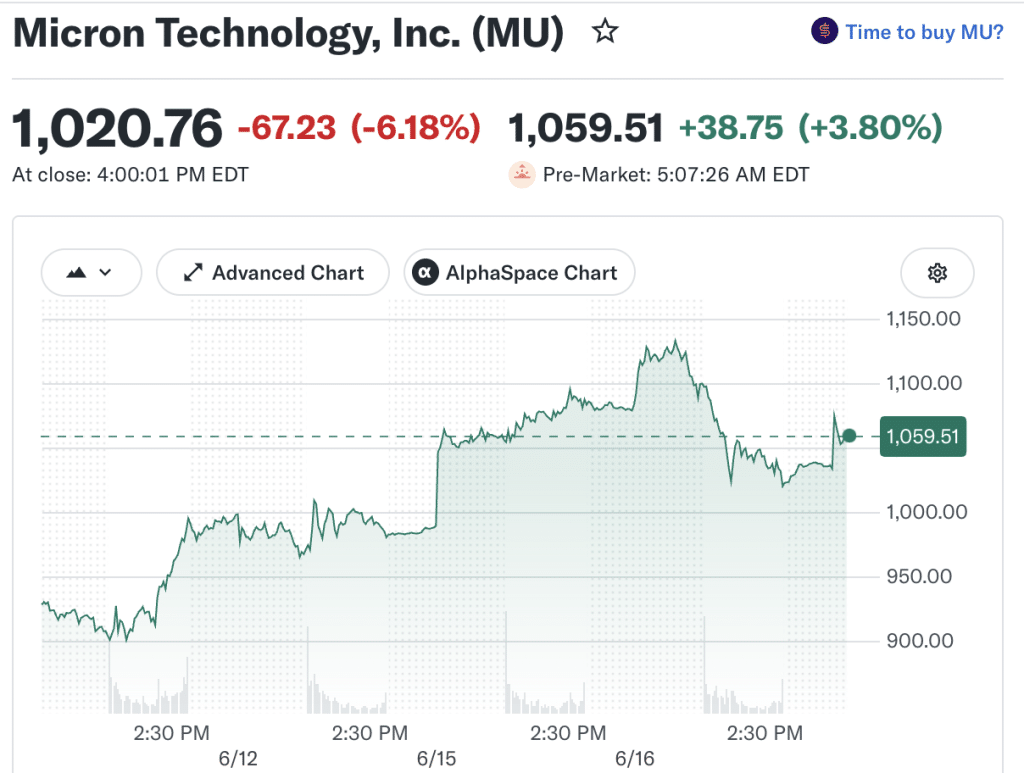

Micron has gained more than 900% over the past year and briefly crossed the $1 trillion market-cap mark. It has emerged as one of the biggest beneficiaries of the AI spending boom. Yet ahead of Micron’s earnings on June 24, analysts are publishing some of the widest forecasts seen anywhere in large-cap tech. Analysts seem to remain divided on whether this rally is still unfolding or already nearing its limits.

Also Read: Peter Thiel’s Leaked Dialog Retreat Attendees Worth 68% More Than the Pentagon’s Budget

The argument starts with high-bandwidth memory. These are chips used along with Nvidia and AMD’s AI accelerators. Micron says its HBM supply for 2026 is already sold out, and demand across the sector remains strong. Goldman Sachs recently raised its estimate for the DRAM supply deficit next year to 4.9%. It describes it as the deepest shortage the memory industry has seen in roughly 15 years. Despite this, the bank kept a Neutral rating on the stock after lifting Micron’s stock price target to $900.

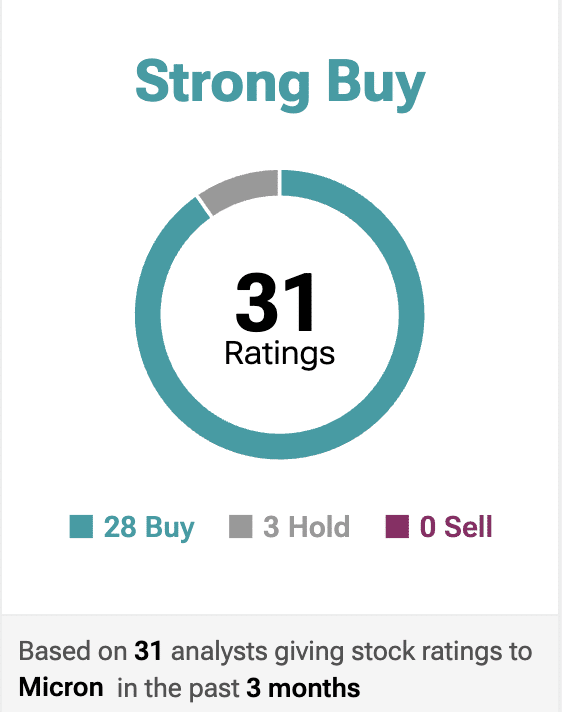

On the contrary, TD Cowen raised its target to $1,500. RBC Capital moved to $1,200. Aletheia Capital went even further, setting a $1,600 target and arguing that HBM pricing could more than double by 2027 as AI infrastructure spending accelerates. Susquehanna currently holds the highest published target at $1,750. In addition, data from TipRanks suggests a “Strong Buy” signal.

Part of this bullishness comes from a belief that memory is becoming far more valuable in AI systems than it was during previous chip cycles. Aletheia estimates memory could account for more than 70% of AI hardware value by 2027, up from roughly the mid-40% range today.

Some investors point to comments Micron CEO Sanjay Mehrotra made earlier this year. He said memory supply would not catch up with demand until 2028. The remark has gained fresh attention as HBM shortages continue and Micron’s 2026 supply remains sold out. These comments came when Micron was trading below $500. Since then, the stock has more than doubled.

Also Read: BlackRock’s First Bitcoin Yield ETF Launches Today as XRP Whales Control 74.1% of Supply

The bearish side isn’t really about whether AI demand is real. Most analysts agree it is. The disagreement is over how much of that future has already been priced into the stock.

Morningstar’s fair-value estimate sits near $455. 24/7 Wall St. maintains a sell rating with a $435.15 target. According to S&P Global data, one active target still stands as low as $249.

There are other reasons investors remain cautious. Micron shares have already pulled back from recent highs, and CEO Sanjay Mehrotra disclosed 25 separate stock sales during May. While insider selling doesn’t automatically signal trouble, it hasn’t gone unnoticed with the stock sitting near record levels.

This leaves the upcoming earnings report as the next reality check. Analysts expect roughly $34 billion in revenue and nearly $19.5 in earnings per share. After a 900% run, the numbers alone may not be enough. Investors will be listening even more closely to what management says about pricing, supply constraints, and demand heading into 2027.

Also Read: Morgan Stanley Slashed Its Oil Forecast as Nvidia Led a $40B Debt Rush on the Iran Deal