Markets

July 15, 2026

Trump’s Worst Crypto Nightmare? Japan Just Cleared the Way for Bitcoin ETFs

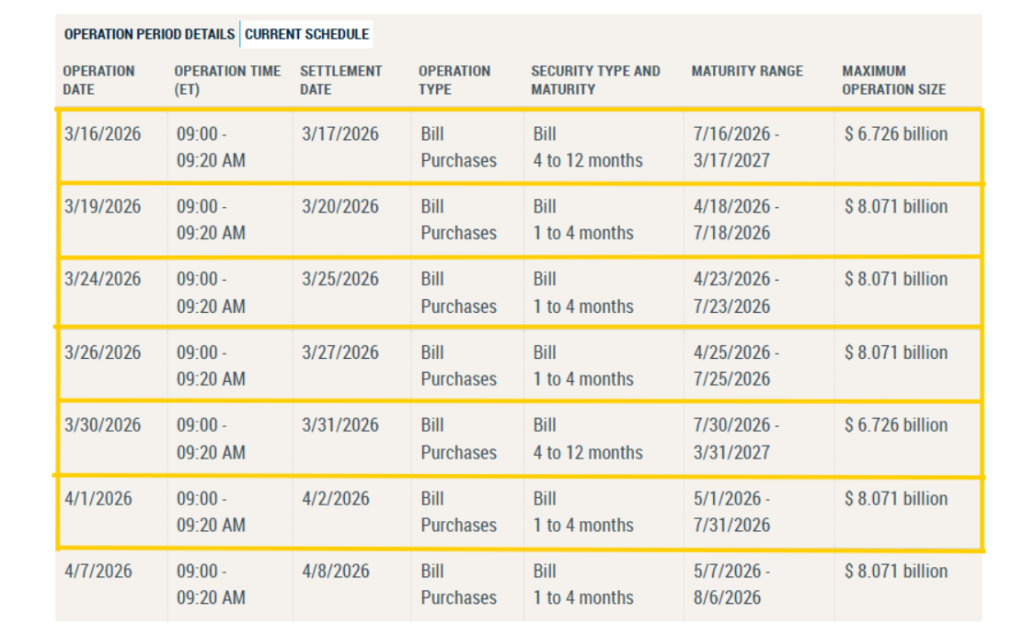

Wednesday’s rate decision from the Fed lands in the middle of the most complex macro week of 2026. The Federal Reserve is widely expected to hold rates at 3.50%–3.75%, with CME FedWatch showing over 92% probability of a pause. But the hold itself is almost beside the point. US inflation is climbing again as Iran war oil prices keep pushing energy costs higher, and a Fed rate cut looks increasingly impossible because of it. Monday’s liquidity injection of $6.72 billion already signals backstop behavior before Powell says a word. The BOJ rate decision Thursday adds even more weight to a week that has no slow moments.

Also Read: Goldman Warns 25% Recession Risk as $150 Oil Hits US, Europe, and Asia

@Xaif_Crypto stated:

“The Fed is buying $47 BILLION dollars in Treasury Bills over the next 2.5 weeks. Every single week. Like clockwork. More liquidity in the system means more fuel for the next $XRP pump.”

That Fed liquidity injection runs like clockwork week after week. The 2-year Treasury yield is also trading above the Fed effective rate by the widest margin since 2023, suggesting markets are already pricing something the Fed hasn’t said out loud yet.

Also Read: Trump’s $65B Iran War Could Have Ended Homelessness and Rebuilt Gaza

Bloomberg stated:

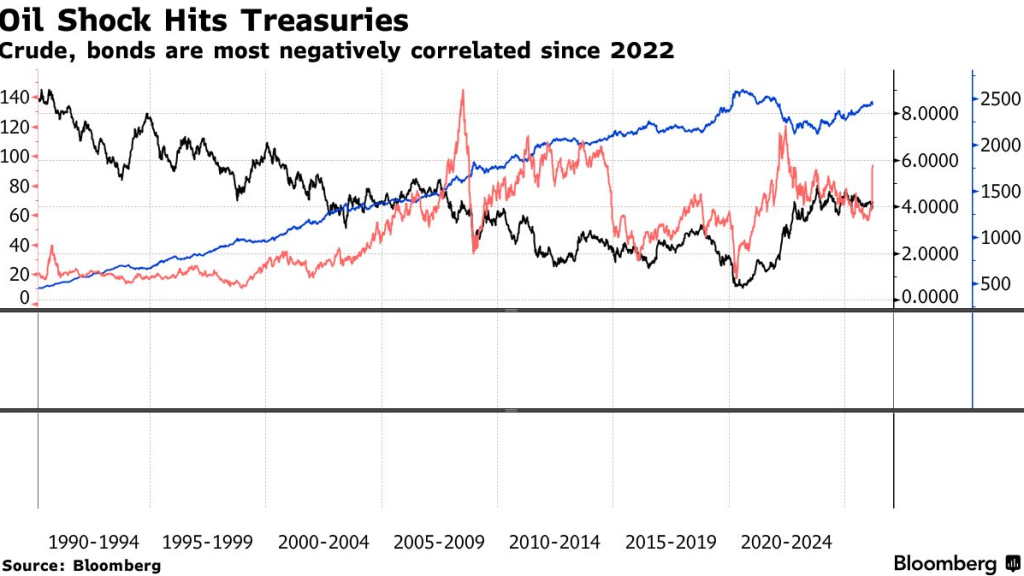

“Bond investors are starting to ponder whether the inflation worries sparked by the Iran war will soon tip over into concern about the risk to economic growth from elevated oil prices.”

Any Fed rate cut is off the table as long as the Iran war keeps oil elevated and Truflation’s real-time CPI sits at its year-to-date high. But markets are repricing growth risk just as fast. Crude and bonds have hit their most negative correlation since 2022, and Iran war oil prices are now moving Treasuries in both directions at once.

The dot plot matters more than the rate call itself this week. The current median shows one 25bp cut for 2026, and if that moves to zero, markets will read stagflation. A Fed rate cut looks even less likely with core PCE still at 2.8%, well above the 2% target, and February CPI expected to show another energy-driven uptick from the Iran war.

Also Read: Iran Official: Hormuz May Reopen Only if Oil Is Traded in Chinese Yuan

This week’s liquidity injection activity suggests the Fed is aware of tightening financial conditions, but Powell’s 2:30 PM press conference is where the real signal comes from. With the BOJ rate decision landing the very next day, there is no room for Powell to leave any ambiguity on Wednesday.

Written by Vladimir Popescu

Vladimir Popescu leads editorial coverage at BlockNow, with over 8 years in financial and tech journalism. He previously held editorial leadership roles at Watcher Guru and Windows Report, and has been cited by Forbes for his crypto market coverage.