Markets

July 5, 2026

German Draft Budget Eyes Over €203 Billion in New Borrowing

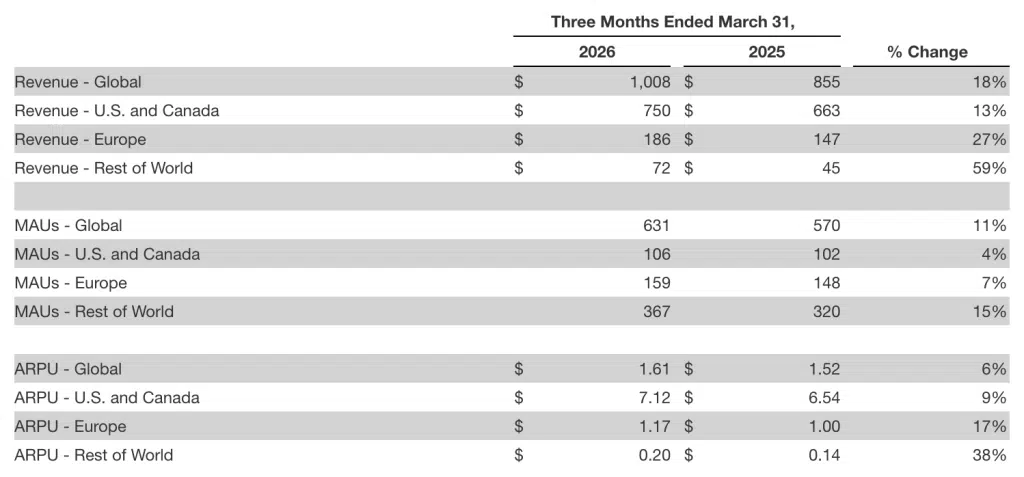

Pinterest’s Q1 earnings came in better than expected. The company reported $1.008 billion in revenue, which is up 18% year over year. This was ahead of estimates of about $965 million. Adjusted earnings per share were $0.27, beating the $0.23 consenus. After several uneven quarters, this was a more direct set of results. These were supported by steady user growth and improving ad performance.

Also Read: Iran Strikes UAE’s Fujairah Port, Only Hormuz Bypass Burning, Oil Hits $114

Pinterest ended the quarter with 631 million monthly active users. This is a 11% increase from a year ago. Growth was broad across the regions, with international markets continuing to contribute meaningfully. The company also noted that engagement remains strong. More than 80 billion searches were reported on the platform each month. Several of these were tied to shopping-related intent. Bill Ready, CEO of Pinterest, added,

“We delivered a strong start to 2026, with Q1 revenue surpassing $1 billion, up 18% year over year, and global monthly active users growing to 631 million, our tenth consecutive quarter of double-digit user growth.”

This has further started to show up in revenue. Pinterest’s Performance+ ad tools, which use AI for targeting and bidding, now account for about 20% of lower funnel revenue. The firm said these tools also helped balance out weaker spending from large retail advertisers earlier in the quarter.

Also Read: Palantir Q1 Earnings: Revenue Soars 85% to $1.63B, Karp Puts Defense First

Another key part of the quarter was capital return. Pinterest said it completed around $2 billion in share repurchases so far this year. This included about 109 million shares bought at an average price near $18. As a result, the company reduced its share count by about 16% compared with the previous quarter.

This move is closely tied to Elliot Investment, which disclosed a $1 billion stake in March. It is now the company’s largest shareholder. The firm has been involved with Pinterest since 2022, with partner Marc Steinberg already on the board. The buyback was partly funded through a $1 billion convertible note, along with existing cash. Ready added,

“We are excited to continue our partnership with Elliott for the next phase of Pinterest’s growth. Elliott’s investment is a strong vote of confidence in the work we have done to build our business and the significant opportunities ahead for Pinterest.“

Pinterest still has about $2 billion remaining under its total $3.5 billion buyback authorization. The Pinterest stock price showed sharp volatility around the earnings release, briefly spiking before settling closer to the $20–$21 range.

On profitability, adjusted EBITDA came in at $207 million with a 20% margin, in line with last year. Free cash flow was at $312 million. But the company reported a GAAP net loss of around $74 million, compared with a profit in the same period last year.

Ad impressions increased 24% year over year. Meanwhile, pricing declined about 5%. The firm said pressure from large retail advertisers remained, though AI-based improvements helped ease some of that impact later in the quarter.

For the second quarter, Pinterest expects revenue between $1.13 billion and $1.15 billion. This is slightly above analyst estimates and suggests continued momentum in Pinterest revenue growth.

Despite the earnings beat, the Pinterest stock price saw only limited movement after the results. The muted reaction shows that investors are still looking for consistent execution over a longer period.

Also Read: Tether Buys 132 Tonnes Gold Worth $19.8B, Outbuying Fed ECB BoE

Written by Sahana Kiran

Sahana Kiran has been covering financial markets since 2019, with a focus on cryptocurrencies, fintech, and the geopolitical events shaping them. She previously reported for AmbCrypto and Watcher Guru, and now writes for BlockNow.