Markets

July 18, 2026

Alphabet Q2 Earnings: Analysts Project 24% Profit Growth Amid AI Cloud Surge

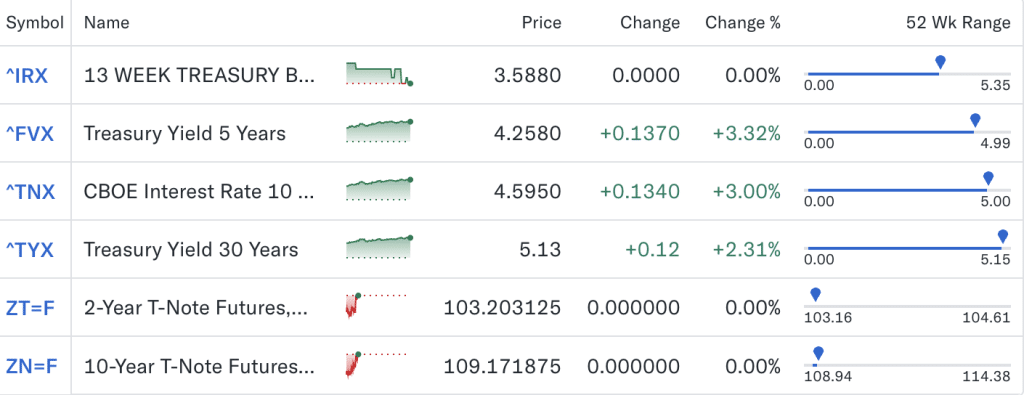

The US bond market remained under pressure this week as Treasury yields moved higher. Investors questioned whether the Federal Reserve’s inflation fight is falling behind. The 10-year Treasury yield recently climbed to 4.63%. Meanwhile, the 30-year yield stayed above 5%. This reflected continued concerns around inflation and borrowing costs. Kevin Warsh, who officially took over as Fed chair following his Senate confirmation, now faces a market that is increasingly skeptical that the Federal Reserve’s inflation fight is close to ending.

Also Read: The Smartest Money on Earth Sold $8B in Microsoft and Cut Nvidia 93% in Q1

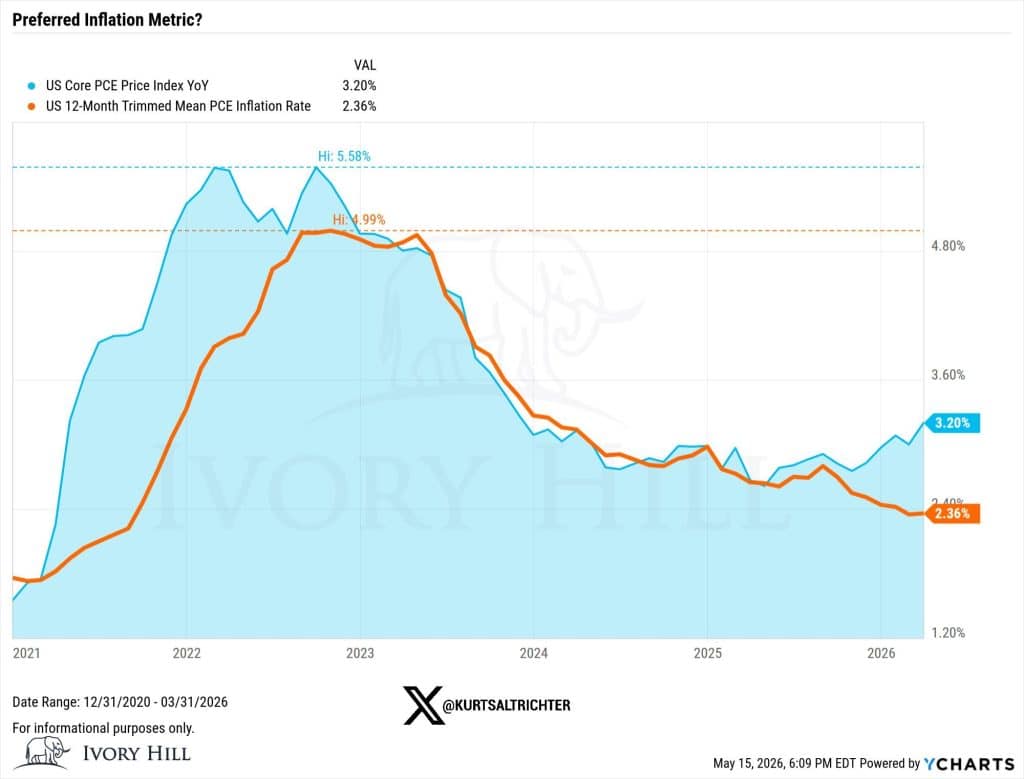

Kevin Warsh has indicated support for using Trimmed Mean PCE as a broader inflation measure instead of relying primarily on Core PCE. This has been the Fed’s preferred gauge for more than two decades.

The two measures currently show very different readings. Core PCE is running around 3%, while Trimmed Mean PCE is closer to 2.3%. The trimmed measure removes the largest monthly price swings rather than excluding categories like food and energy entirely.

The shift is important because inflation data directly affects expectations around Fed rate cuts and broader market policy decisions.

According to reports, some economists and banks have warned that changing the preferred inflation measure could create confusion for markets, particularly while price pressures remain elevated across several sectors.

Also Read: Strong Japan Q1 GDP Could Bolster Yen Exchange Rate Stability

Bond market investors are increasingly signaling that the Fed may still be behind the curve on inflation. Ed Yardeni, president of Yardeni Research, noted that the 2-year Treasury yield is now trading above the federal funds rate. This is often viewed as a sign that markets expect tighter monetary policy ahead. Yardeni further wrote,

“The market is signaling that the current FFR is too low to curb inflation and may have to be hiked.”

Recent inflation data has added to those concerns. April CPI rose 3.8% year over year, while wholesale inflation increased 6%. This marks its fastest pace since 2022.

Higher Treasury yields have also kept pressure on the housing market. Freddie Mac recently showed average 30-year mortgage rates remaining above 6%. In addition, Zillow data placed some 30-year fixed loans near 6.27%.

Analysts expect mortgage rates in 2026 to remain elevated unless inflation cools more consistently or bond yields begin moving lower.

Also Read: Bitcoin Dip Defied by Intesa Sanpaolo’s $235M ETF Expansion

Written by Sahana Kiran

Sahana Kiran has been covering financial markets since 2019, with a focus on cryptocurrencies, fintech, and the geopolitical events shaping them. She previously reported for AmbCrypto and Watcher Guru, and now writes for BlockNow.