Markets

July 20, 2026

Oracle’s $42 Billion Deficit Is What Goldman’s AI Credit Blowout Warning Looks Like

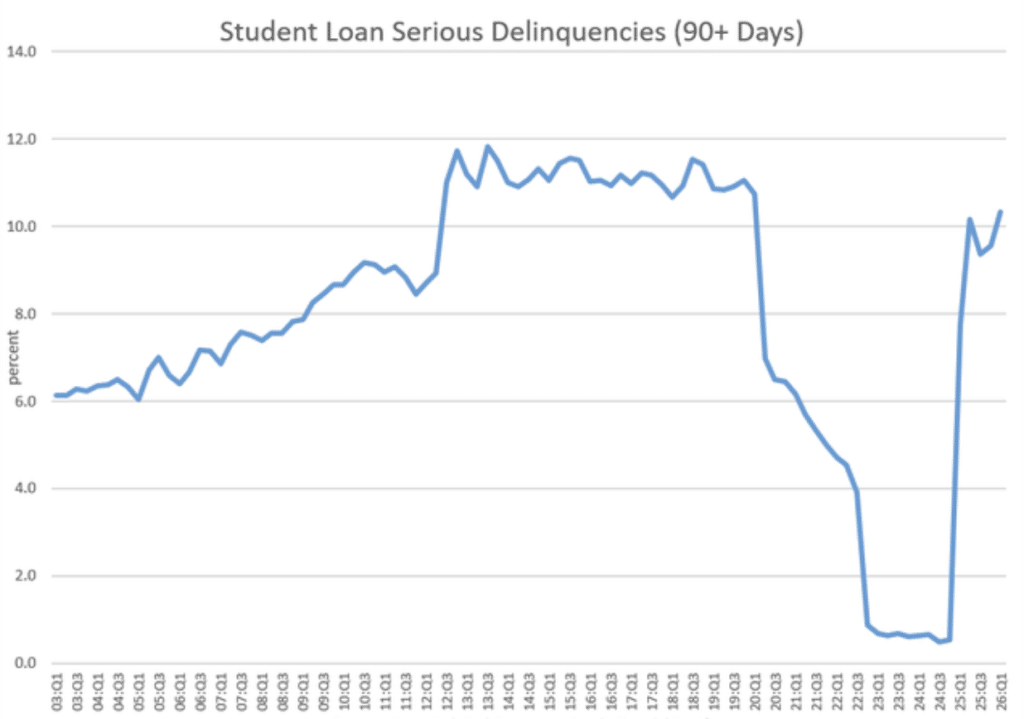

The US student loan debt problem is starting to look less like a temporary post-pandemic hangover and more like a long-term financial strain spreading across middle-income households. Delinquent balances tied to federal student loans climbed to a record $171.4 billion in the first quarter of 2026, according to New York Fed data. Meanwhile, millions of borrowers slipped deeper into financial trouble after repayment protections expired. What stands out now is who is falling behind and how quickly the numbers are accelerating again.

Also Read: Iran Launched a $10B Bitcoin Platform at Hormuz After America Froze $344M

The latest figures from the Federal Reserve Bank of New York show roughly 2.6 million borrowers entered student loan default in Q1 2026. This was following another 1 million defaults in late 2025. This pushed the seriously delinquent rate on federal student loans to 10.3%. It is the highest level since early 2020.

This phase of the student debt crisis is increasingly affecting older Americans rather than recent graduates. The average borrower entering default is now close to 40 years old, up from 36 before the pandemic. New York Fed researchers also found many of these borrowers had been current on payments before COVID disrupted repayment schedules and paused collections.

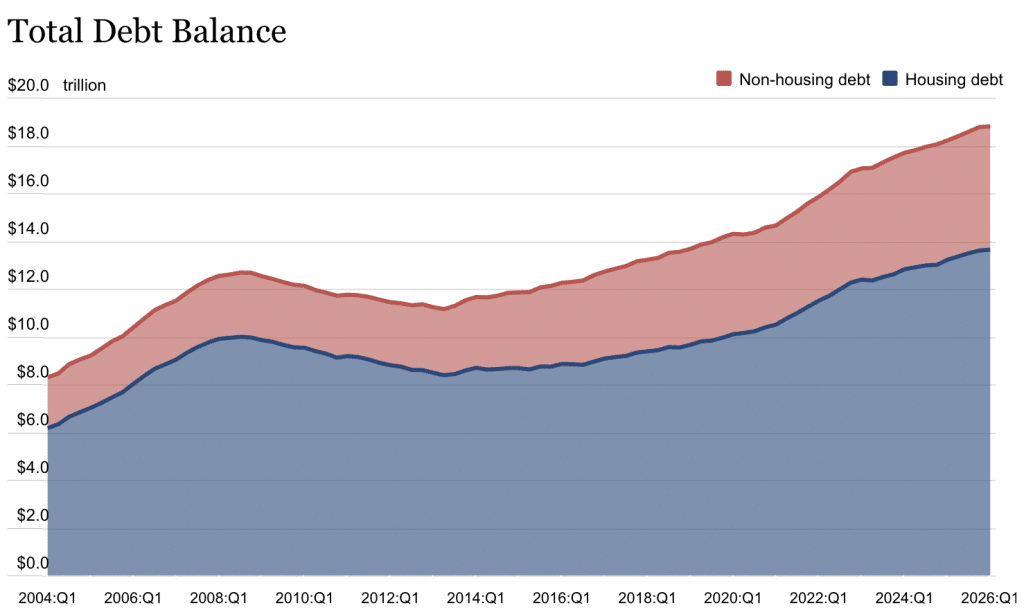

Federal student loans now total nearly $1.7 trillion across 42.8 million Americans. This is with average balances approaching $40,000. Student loan debt also represents around 30% of all non-mortgage consumer debt in the country.

Also Read: Kevin Warsh Can’t Beat Inflation so He Is Changing How the Fed Measures It

Part of the problem traces back to the repayment restart process. Payments resumed in late 2023 after the pandemic pause. But the Biden administration’s temporary “on-ramp” program delayed credit reporting consequences for missed payments until late 2024. Many borrowers never fully returned to regular payments once protections expired.

The New York Fed said nearly 40% of borrowers entering default are also behind on other bills. This includes auto loans, mortgages, and credit cards. Researchers warned the pressure could worsen as collections restart and borrowers in the now-defunct SAVE repayment plan move back into repayment later this year.

At the same time, the federal government is still struggling to organize collections. The Education Department has shifted parts of the federal student loans system to the Treasury Department. Meanwhile, staffing cuts and restructuring continue to create confusion for borrowers trying to navigate repayment options.

Also Read: The Smartest Money on Earth Sold $8B in Microsoft and Cut Nvidia 93% in Q1

Written by Sahana Kiran

Sahana Kiran has been covering financial markets since 2019, with a focus on cryptocurrencies, fintech, and the geopolitical events shaping them. She previously reported for AmbCrypto and Watcher Guru, and now writes for BlockNow.