Markets

July 29, 2026

US Treasury Buys Back $2B as US Debt Nears $40T, Margin Debt Climbs at Dot-Com Era Pace

Key Takeaways

The IRS COVID refund deadline is tomorrow, and that one date decides whether tens of millions of people keep their shot at a COVID tax penalty refund or lose it for good. As Taxpayer Advocate reveals, relief is not automatic, so nobody should assume a check is coming without lifting a finger. This also comes at a time when plenty of taxpayers are still waiting on their refunds from the regular 2026 filing season, so a second refund fight landing on top of that is not exactly welcome news.

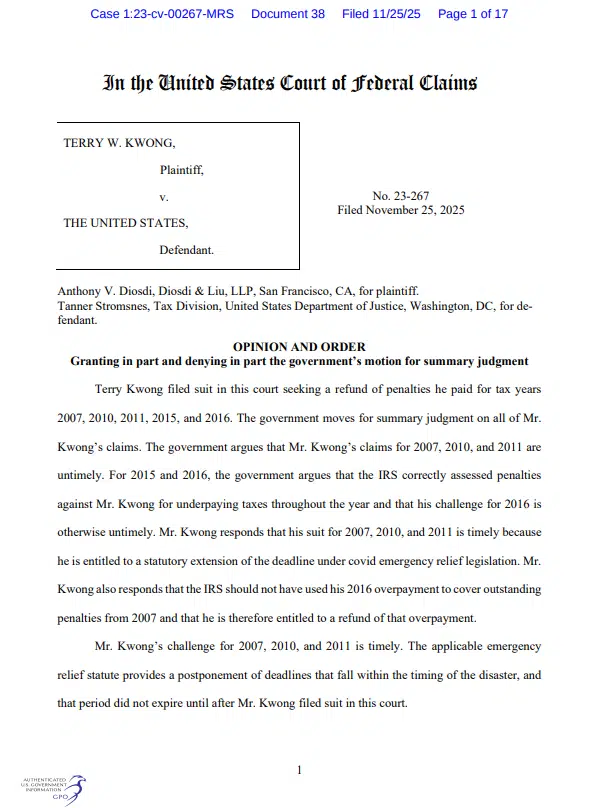

A federal court ruled, in Kwong v United States, that the IRS should never have charged penalties or interest on returns filed or paid late during the pandemic, since the law had already postponed those deadlines the whole time, whether the IRS treated them that way or not. An eligible IRS pandemic refund can reach up to $1,700 per taxpayer, and the fix is a Form 843 refund claim, filed electronically or mailed with a postmark by tomorrow.

That single step is what keeps the IRS COVID refund deadline from quietly closing on a claim nobody got around to filing. Right now, the IRS is not issuing a single check, and it will not budge the IRS COVID refund deadline for anyone who misses it.

Also Read: Blue Cross Blue Shield Overcharged $2.67B and You May Be Owed $333

Back in November 2025, the U.S. Court of Federal Claims decided Kwong v United States and found that Section 7508A(d) of the tax code required an automatic postponement of pretty much every federal filing and payment deadline between January 20, 2020, and July 10, 2023. That’s the entire COVID-19 disaster window, and also the reason the IRS COVID refund deadline exists at the time of writing. That single ruling ended up touching a few different kinds of claims at once, not just one flat category of penalty, and it helps to see how those break down before getting into the paperwork.

The IRS spent those years assessing failure-to-file penalties, failure-to-pay penalties, and interest on returns it was treating as late. Under Kwong v United States, none of that was actually late.

National Taxpayer Advocate Erin Collins has laid this reasoning out publicly more than once, and her comments further down explain why the IRS COVID refund deadline matters this particular week and not some vague point down the road. It’s an odd thing to have a refund deadline at all, but here it is.

| Claim Type | What It Covers | Why It Matters |

|---|---|---|

| Late-Filing And Late-Payment Penalties IRC §6651(a)(1) and §6651(a)(2) | Penalties tied to a deadline inside the COVID disaster window | Strongest case, since the law postponed those deadlines by statute |

| Underpayment Interest No separate IRC section, tied to the same postponement | Interest that accrued on unpaid tax during the same window | Smaller share of claims filed, but often the larger dollar amount |

| Limitations-Period Arguments Governed by IRC §6511, not §7508A(d) | Claims that looked time-barred under the IRS’s normal three-year rule | The main reason tomorrow’s cutoff exists at all |

Individuals, small businesses, corporations, estates, and even trusts can pursue an IRS pandemic refund if they paid a failure-to-file penalty, a failure-to-pay penalty, an estimated tax penalty, or interest tied to a deadline that landed between January 20, 2020, and July 10, 2023. That covers tax years 2019 through 2022 for most filers, and also a fair number of expats and small business owners who got hit during the same stretch.

Even someone who owed zero tax but still got a late-filing penalty might have a real COVID tax penalty refund case, since the return technically wasn’t late once you apply the postponed deadline. A lot of people assume an IRS pandemic refund only applies to individuals, but it doesn’t, and that’s worth repeating.

Nobody needs an exact number to file a Form 843 refund claim or start a COVID tax penalty refund case. A protective claim just has to name the taxpayer, the year, and the legal basis found in Kwong v United States, and that’s honestly most of the work.

Also Read: JPMorgan, BofA, Wells Fargo, and PNC Are Quietly Buying Their Way Out of Your Debit Fee Cap

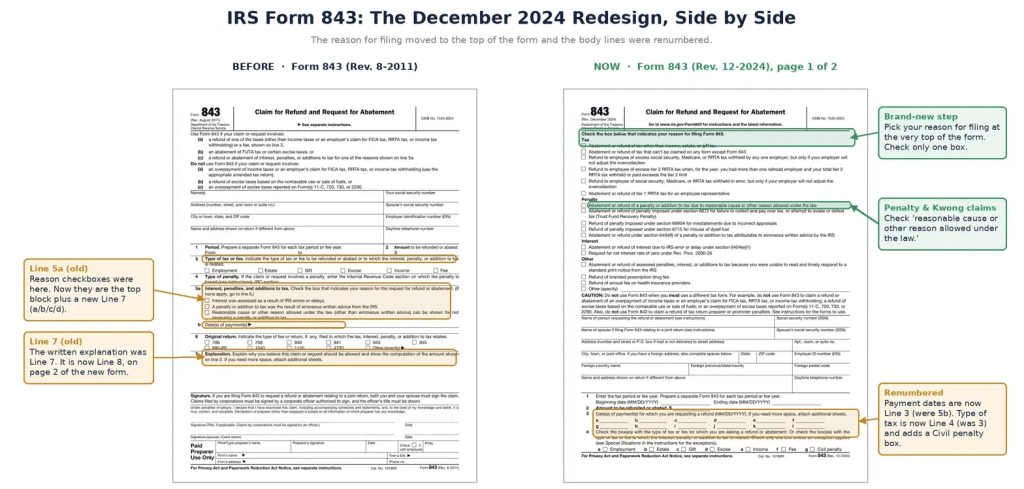

Most people are still going to mail this one in. Form 843 has never really worked as an e-file form, and that hasn’t changed for most reasons people use it in the first place.

Since July 1, an individual taxpayer with an existing IRS Online Account can submit a Kwong-related Form 843 refund claim electronically, though only for penalties and interest the taxpayer already paid in full.

Everybody else, and that includes most business filers and anyone without an online account, has to mail the paper version, postmarked by tomorrow, to the IRS Service Center in Ogden, Utah, at 1973 N Rulon White Blvd., Ogden, UT 84201.

Certified mail with a return receipt is basically the only proof of a timely IRS COVID refund deadline filing. That’s also the safest way to protect a COVID tax penalty refund in case processing loses the form somewhere along the way. An IRS pandemic refund claim mailed without any tracking is a gamble nobody really needs to take, not when a receipt costs a few extra dollars.

One more thing worth checking before anything gets mailed out: the IRS redesigned Form 843 in December 2024, moving the reason-for-filing checkboxes to the top of the page and renumbering half the lines on it. A copy pulled from an old bookmark or a saved PDF from a few years back will not match what the current version actually looks like. Filling in the wrong line can slow the whole Form 843 refund claim down.

Across the top, write “Protective Refund Claim Pursuant to Kwong Case.” That single line is what tells the IRS to route the filing correctly instead of letting it sit in a general penalty pile somewhere. On the current version of the form, check the penalty abatement box near the top, just above the name fields.

Fill in the tax period, an amount if it’s known, and the payment date if the taxpayer already paid the penalty. The written explanation goes on Line 8, and it needs to name both Section 7508A(d) and Kwong v United States as the legal basis for the claim.

One form covers one tax year, so a taxpayer with penalties spread across 2020, 2021, and 2022 needs three separate forms, each one filed before the IRS COVID refund deadline shuts the door. It’s a bit tedious filling out three copies of the same form. However, a Form 843 refund claim done three times is still faster than losing an IRS pandemic refund altogether.

National Taxpayer Advocate Erin Collins stated:

“By the court’s logic, the IRS should not have assessed penalties for late filing or payment during that 3.5-year period, nor charged interest on those amounts.”

Filing before the IRS COVID refund deadline doesn’t put a dime in anyone’s account this month, or probably this year either. The IRS disagrees with Kwong v United States and is appealing it. Therefore, every COVID tax penalty refund is on hold until that appeal actually plays out in court.

It doesn’t help that Where’s My Refund isn’t updating for a lot of regular filers either, so patience is already running thin before this Kwong situation even enters the picture.

Tax attorney Alyssa Maloof Whatley, a director at Frost Law, told CNBC Select that the case could stretch on for years. A claim filed near the IRS COVID refund deadline is just a place in line rather than a payout landing in the mail. An IRS pandemic refund and a COVID tax penalty refund are basically the same thing, just two different names for it. Even more, neither one is arriving before the appeal wraps up.

Tax attorney Alyssa Maloof Whatley said:

“It may be a drawn-out case with multiple plaintiffs that takes years to resolve.”

She was also blunt about what happens to anyone who skips a COVID tax penalty refund claim, and doesn’t bother filing at all:

“If you don’t file, you won’t be eligible for any benefit.”

The date isn’t an arbitrary IRS habit. The law generally gives taxpayers three years from the original filing date to claim a refund. It also allows two years from the payment date, whichever is later.

Under Kwong v United States, the postponed deadlines run through July 10, 2023. That means the three-year window for a related Form 843 refund claim expires exactly three years later. Tomorrow marks the IRS COVID refund deadline.

Also Read: Millions of Americans Could Claim IRS COVID Tax Refund Before July 10 Deadline

Erin Collins has also pointed out that the reasoning behind the IRS COVID refund deadline reaches further than penalties alone, touching missed credits and even a few refund claims that people figured had closed a long time ago. A Form 843 refund claim tied to a Kwong v United States argument doesn’t have to be complicated, it just has to land on time.

| Your Situation | Deadline | What To Do |

|---|---|---|

| Already Paid The Penalty | July 10, 2026 | File Form 843 as a refund claim |

| Penalty Assessed But Not Paid | No Fixed Cutoff | File Form 843 as an abatement request instead |

| Filed Or Paid From Overseas | July 10, 2026 | Same Form 843, mailed or e-filed via IRS Online Account |

| Missed A 2019-2022 Refund Entirely | Case-By-Case | Check whether the postponement kept that window open |

National Taxpayer Advocate Erin Collins stated:

“Even though the law is still developing, many taxpayers may need to act on or before July 10, 2026, to protect potential refund rights while the courts continue deciding these issues.”

Anyone who paid a penalty or interest charge between January 2020 and July 2023 has a decent reason to pull their IRS transcript today, not after the IRS COVID refund deadline has already come and gone. No IRS pandemic refund shows up on its own, a Form 843 refund claim has to go in first, and the IRS is not exactly mailing out reminders about any of this.

It also helps to know when to expect your refund on the regular side of things, since the two processes run on completely separate timelines and nobody wants to mix them up.

After tomorrow, the door on this particular COVID tax penalty refund closes for good, regardless of how Kwong v United States is eventually decided on appeal, and that part is not going to change. This is the IRS COVID refund deadline in a nutshell, and it is also the last day anyone gets to argue for it.

Written by Vladimir Popescu

Vladimir Popescu leads editorial coverage at BlockNow, with over 8 years in financial and tech journalism. He previously held editorial leadership roles at Watcher Guru and Windows Report, and has been cited by Forbes for his crypto market coverage.