Markets

July 11, 2026

DXY USD Strength Pressures EUR and Global Peers

Key Takeaways

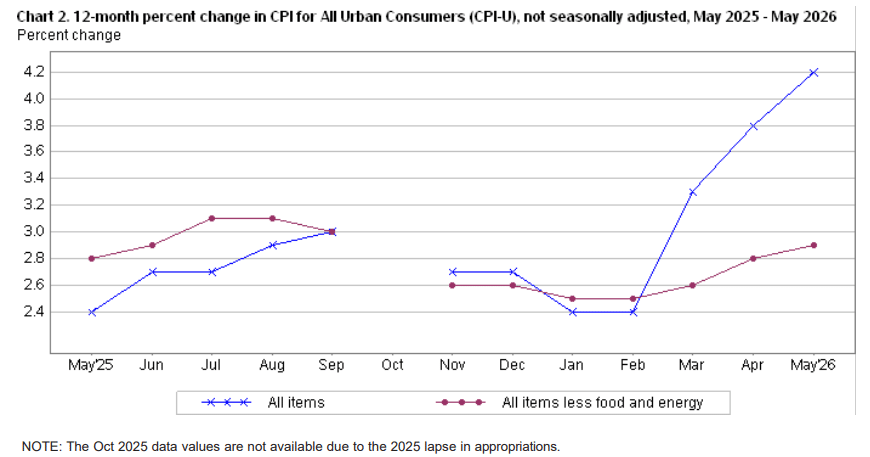

US inflation data takes center stage next week with CPI on Tuesday and PPI on Wednesday. Economists expect headline CPI around 4.2% year-over-year while core stays near 2.9%. These readings will shape Fed rate outlook under Chair Warsh, who signaled hawkish concerns over AI-driven costs. Softer oil prices ease some pressures temporarily. Investors seek clues on possible rate holds or hikes

Also Read: DXY USD Strength Pressures EUR and Global Peers

Economists forecast US inflation data to hover near 4.2% year-over-year when the June CPI lands Tuesday. Analysts expect a 0.5% monthly gain in headline prices with services costs showing particular resilience. Core inflation trends will draw sharp focus as they exclude volatile items and reveal underlying momentum.

The upcoming CPI PPI release will test whether disinflation has truly stalled across production chains. As previously reported by BlockNow, the Federal Reserve’s worst nightmare materialized with sticky May CPI figures that already delay rate cuts and complicate policy planning. Investors now hunt for fresh Warsh policy signals in the data.

Chair Warsh watches these releases closely for evidence of persistent cost pressures across key sectors. Markets adjust their Fed Rate Outlook in real time ahead of the numbers. Stronger readings could reinforce a cautious stance from policymakers through the second half of the year and support limited easing expectations.

Also Read: Japan Pension Shift Triggers 0.6% Yen Rally Amid Fiscal Pressures

Some analysts see early signs that cooling pressures could modestly ease the Fed rate outlook in coming months. Softer demand in certain goods categories may soon flow through the pipeline. Traders will watch the upcoming CPI PPI release for confirmation of any moderation.

Core inflation trends remain the key barometer for sustained progress. Chair Warsh and colleagues pay close attention to these shifts when forming views. Recent warsh policy signals left room for adjustments if data cooperates. Policymakers could gain flexibility to assess conditions more patiently.

Markets already price in limited easing later this year. US inflation data will help determine whether these cooling signals strengthen. A softer-than-expected print might encourage officials to hold steady rather than tighten further. This scenario would support gradual normalization without rushing decisions. Investors monitor every detail for clues on the policy path ahead.

Also Read: Record Activity Fuels Goldman Q2 Earnings Optimism

Written by Carlos Terenzi

Carlos Terenzi is a financial analyst with over 10 years of experience in crypto, finance, and international relations, focusing on Bitcoin, monetary policy, and precious metals.