Business

July 28, 2026

Johnson & Johnson’s $5.5B Talc Settlement: Could You Qualify for a Payout?

The upcoming March Employment Data release will determine market sentiment for the entire spring season. Analysts expect this report to clarify the Fed interest rate outlook for the remainder of 2026. If hiring remains robust, the central bank may maintain current rates to ensure price stability. However, moderate growth would support a case for easing soon. Traders are positioning their portfolios now to prepare for any unexpected volatility or growth signals.

Also Read: XRP Ledger Gets AI Security Upgrade as Ripple Expands Institutional Use Cases

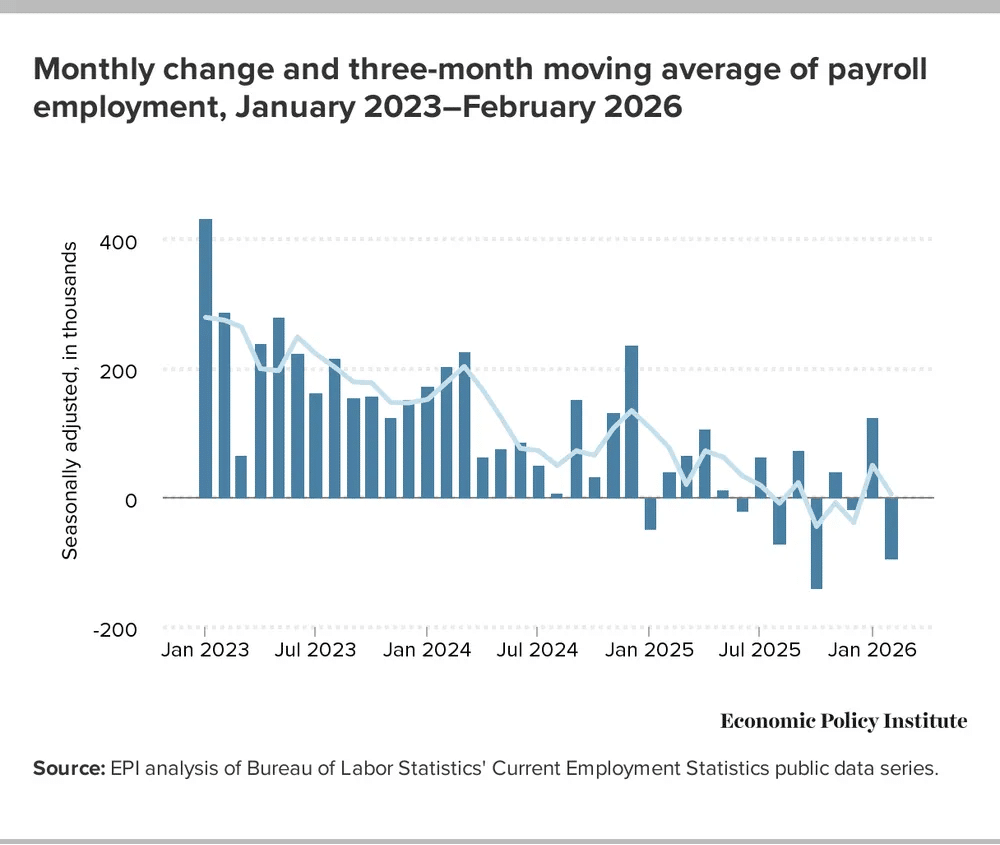

Market participants view the March Employment Data as the ultimate compass for the second quarter. This specific report reveals if job market resilience is fueling consumer spending or cooling down. A “goldilocks” result, steady hiring with moderate wage growth, typically triggers a bullish pivot toward equities. Traders often favor non-farm payroll growth that aligns with a soft-landing narrative.

If the data exceeds expectations, investors may pivot toward a “higher-for-longer” stance. This shift often strengthens the dollar while putting pressure on growth stocks. Conversely, a weaker report could spark a rally in Treasury markets as a dovish Fed interest rate outlook gains steam. Regardless of the direction, the economic labor statistics provide the necessary liquidity and volatility for major portfolio rebalancing.

Institutional desks use these figures to confirm if the primary economic trend remains intact. By analysing the labor participation rate alongside headline numbers, traders determine their risk appetite for the months ahead. Total clarity on the employment front allows for more confident positioning across all major asset classes.

Also Read: Putin’s Oil Revenue Just Hit $760M a Day After the US Issued a Russia Sanctions Waiver

The Fed interest rate outlook remains a centrepiece of market strategy following the central bank’s March decision to hold rates steady between 3.5% and 3.75%. While officials still signal a potential cut later this year, the timeline is increasingly “data-dependent” amid a complex geopolitical landscape. Consequently, the upcoming March Employment Data acts as a critical filter for May’s policy expectations.

Market participants are currently pricing in a modest rebound in non-farm payroll growth after February’s contraction of 92,000 jobs. A positive surprise in the economic labor statistics, such as a return to steady hiring, could reinforce a “hawkish hold.” The Fed prioritizes cooling sticky inflation over immediate easing.

Conversely, if the report reveals cracks in job market resilience, it may validate the recent dissent from Governor Stephen Miran. He favoured an early 25-basis point cut to protect the employment mandate. Ultimately, these labor figures will dictate whether the Fed can navigate a “soft landing” or if further restrictions are necessary.

Also Read: Morgan Stanley’s Bitcoin ETF Is Imminent as Iran War Wipes $3.5T From Stocks

Written by Carlos Terenzi

Carlos Terenzi is a financial analyst with over 10 years of experience in crypto, finance, and international relations, focusing on Bitcoin, monetary policy, and precious metals.