Markets

July 26, 2026

Meta Q2 Earnings Spotlight Shifting Monetization Strategies for Mark Zuckerberg

Key Takeaways

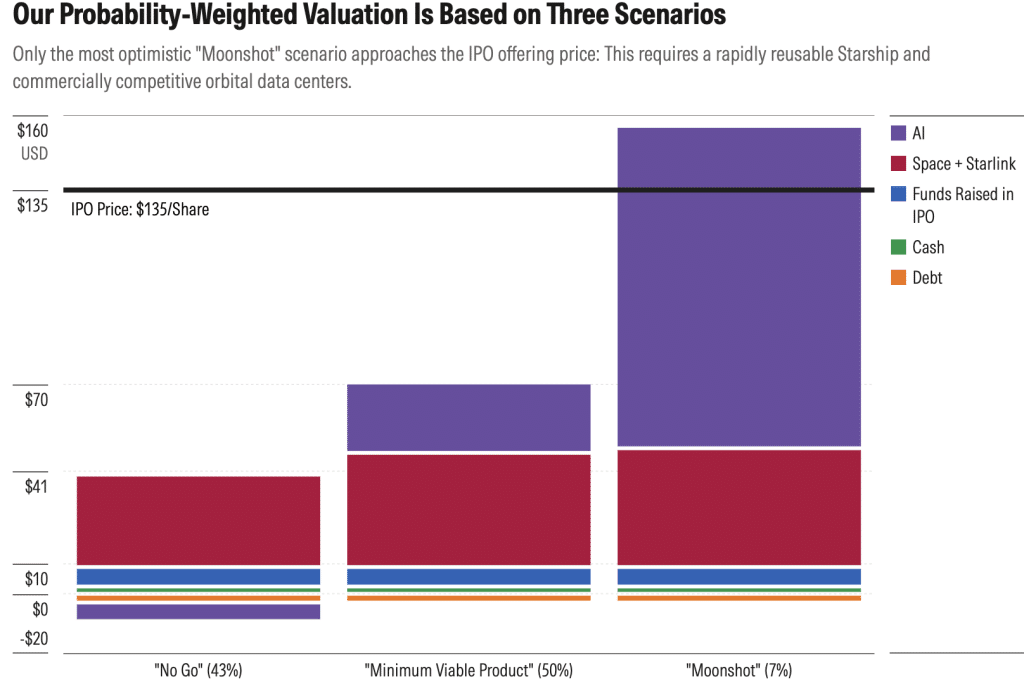

SpaceX is just days away from what could become the largest public listing in market history. But not everyone on Wall Street is convinced the numbers add up. The upcoming SpaceX IPO is expected to value the company at about $1.77 trillion when it begins trading on Nasdaq under the ticker SPCX on June 12. This would place Elon Musk’s company among the largest firms in the US from day one. Yet a new Morningstar analysis argues investors may be paying far more than the business is currently worth. According to the research firm, SpaceX’s valuation should be closer to $780 billion, less than half of its IPO target.

Also Read: Hindenburg Omen Hit 3 Days Straight as BofA Flashes 70% Bear Signals & $2T Was Wiped

The debate around the SpaceX IPO is not really about rockets anymore. Morningstar estimates that SpaceX’s launch business and Starlink account for roughly $611 billion of value. Meanwhile, the rest depends largely on the future success of its AI ambitions.

In a report published ahead of the listing, analyst Nicolas Owens said the company appears “significantly overvalued” at its IPO price. Morningstar’s discounted cash flow model values the company at about $63 per share, compared with the $135 offering price. Owens added,

“We think the company has been significantly overvalued and investors will have opportunities to buy the stock at more attractive levels after the IPO.”

The biggest source of uncertainty comes from xAI. This was folded into the SpaceX ecosystem earlier this year. According to Morningstar, xAI posted an operating loss of $6.36 billion in 2025 despite aggressive spending on Grok and the Colossus data center project. The firm assigned only a 7% probability to its most optimistic “Moonshot” scenario. Meanwhile, it gives a 43% chance of a “No Go” outcome where orbital AI data centers fail to become commercially viable.

Also Read: Iran Hit 3 US Bases & the US Struck 20 Targets as UAE Bets Hormuz Will Never Reopen

While the AI division continues to burn cash, Starlink is producing real revenue. Morningstar estimates the satellite internet business generated $11.3 billion in revenue during 2025 with a 39% operating margin. SpaceX also accounted for 83% of all mass launched into orbit last year. This points out its dominance in the commercial launch market.

Despite this, the gap between the IPO valuation and Morningstar’s estimate is difficult to ignore. Reuters reported that Goldman Sachs, Morgan Stanley, Bank of America, Citi, and JPMorgan are underwriting the deal. This could raise as much as $75 billion. It should be noted that only a small percentage of shares will be publicly available at launch. Some analysts expect the SpaceX stock price to remain elevated in the near term.

But for long-term investors, the bigger question is if the company’s AI projects can eventually justify the trillion-dollar premium being placed on the business today.

Also Read: China Plans $295B AI Data Center Buildout as Race With US Intensifies

Written by Sahana Kiran

Sahana Kiran has been covering financial markets since 2019, with a focus on cryptocurrencies, fintech, and the geopolitical events shaping them. She previously reported for AmbCrypto and Watcher Guru, and now writes for BlockNow.