Business

June 27, 2026

Apple Price Hike Signals a New Era of Expensive Electronics

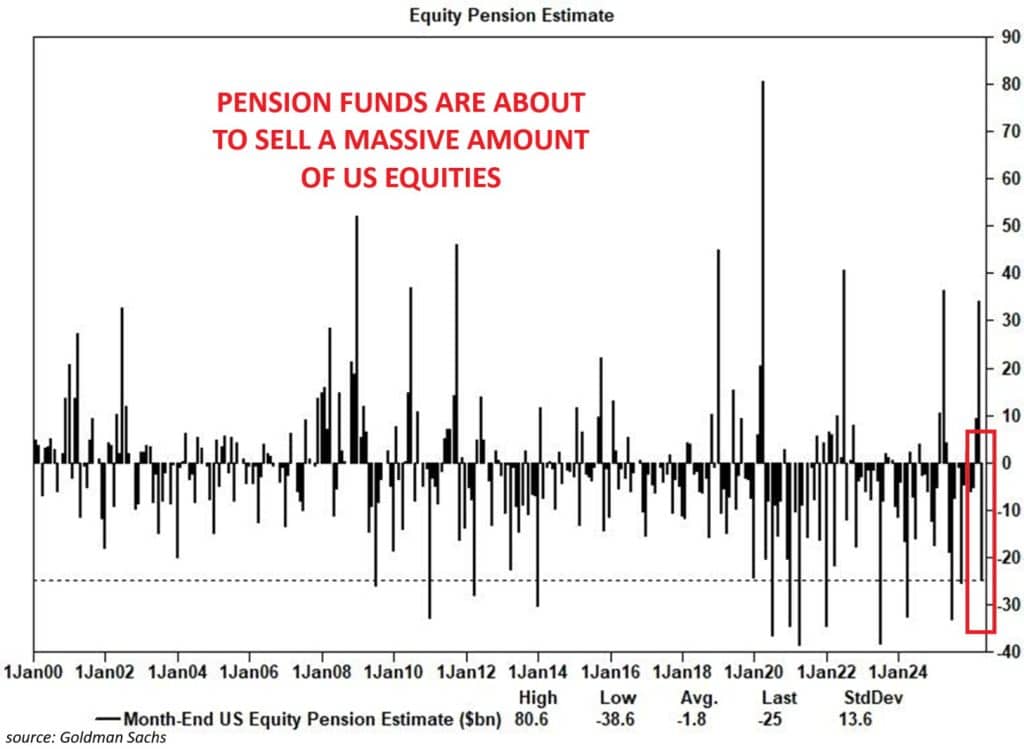

Goldman Sachs estimates that pension funds will sell approximately $23 billion in equities this month, marking the largest non-quarterly selling event on record since 2000. This massive rebalancing, triggered by April’s strong stock market performance, exceeds the previous non-quarterly record by roughly 25% and ranks among the 15 largest monthly sell estimates Goldman Sachs has tracked over the past 25 years. The long-term average monthly pension equity estimate stands at just negative $1.8 billion, meaning this month’s figure is more than 12 times the historical norm.

Also Read: X Money Launch: 6% Savings Crushes Banks as Musk Opens to 600M Users

The selling pressure stems from a stark performance gap between stocks and bonds. The S&P 500 delivered a total return of 8.95% in April, while 10-year Treasuries returned just 0.79%, creating an 8.16 percentage point divergence. This disparity pushed pension fund portfolios out of their predetermined allocation bands, forcing mechanical rebalancing trades. Goldman Sachs initially projected only $2 billion to $3 billion in selling at the start of April, but that estimate surged to $23 billion as the stock market continued climbing throughout the month.

Also Read: Iran Proposes Hormuz Deal to US but Delays Nuclear Talks Until After War

By absolute dollar amount, this rebalancing ranks in the 83rd percentile over the past three years and the 92nd percentile since January 2000. A separate trigger event occurred on April 10, when pension funds sold an estimated $21 billion in stocks, an amount not included in the month-end estimate.

Goldman Sachs also flagged weakening demand from commodity trading advisors as an additional headwind. The combination of fading CTA buying and massive pension fund selling creates potential pressure on equities. Market participants note that pension fund rebalancing is a passive portfolio adjustment rather than an active bearish bet, but the concentrated selling in the short term could still pressure equity indices, particularly with retail investors flooding into equities and institutional investors already stretched on positioning.

Goldman Sachs analysts believe this rebalancing poses significant pressure on U.S. stocks, which are already at fragile highs, especially against a backdrop of rising oil prices. With the stock market at elevated levels and CTAs entering their eighth demand “leg,” the timing of this $23 billion sell wave raises questions about whether a market pullback is overdue.

Also Read: Oil Price: Goldman Raises Brent to $90 as Record Inventory Draws Accelerate

Written by Vladimir Popescu

Vladimir Popescu leads editorial coverage at BlockNow, with over 8 years in financial and tech journalism. He previously held editorial leadership roles at Watcher Guru and Windows Report, and has been cited by Forbes for his crypto market coverage.