Markets

July 28, 2026

How a Robinhood Chain Trader Turned $44K Into Nearly $1M With an Early PONS Bet

Key Takeaways

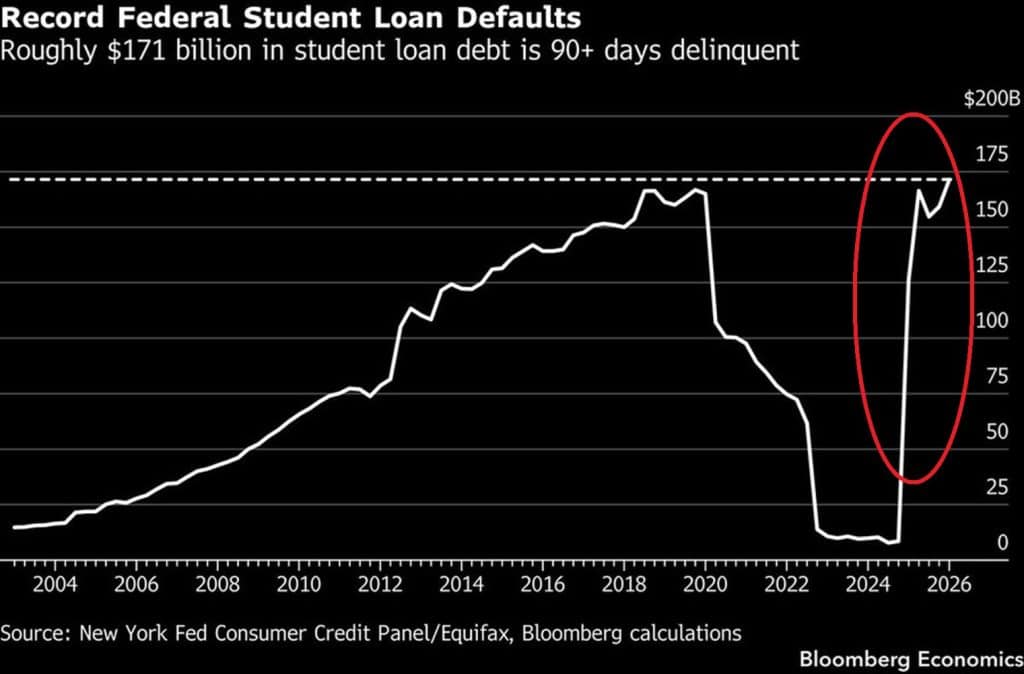

Federal student loan debt in the US climbed to a record $171.4 billion in delinquent balances during the first quarter of 2026. This is a sign that many borrowers are struggling to restart payments after pandemic-era protections ended.

Also Read: Gold Rush Returns as Central Banks, Japan, and Russia Move Billions In Gold

More than 2.6 million borrowers defaulted on federal student loans in Q1 alone. This is up sharply from 1 million in the previous quarter. The average borrower entering default is now nearly 40 years old, according to recent data. This shows the pressure is no longer limited to younger Americans fresh out of college.

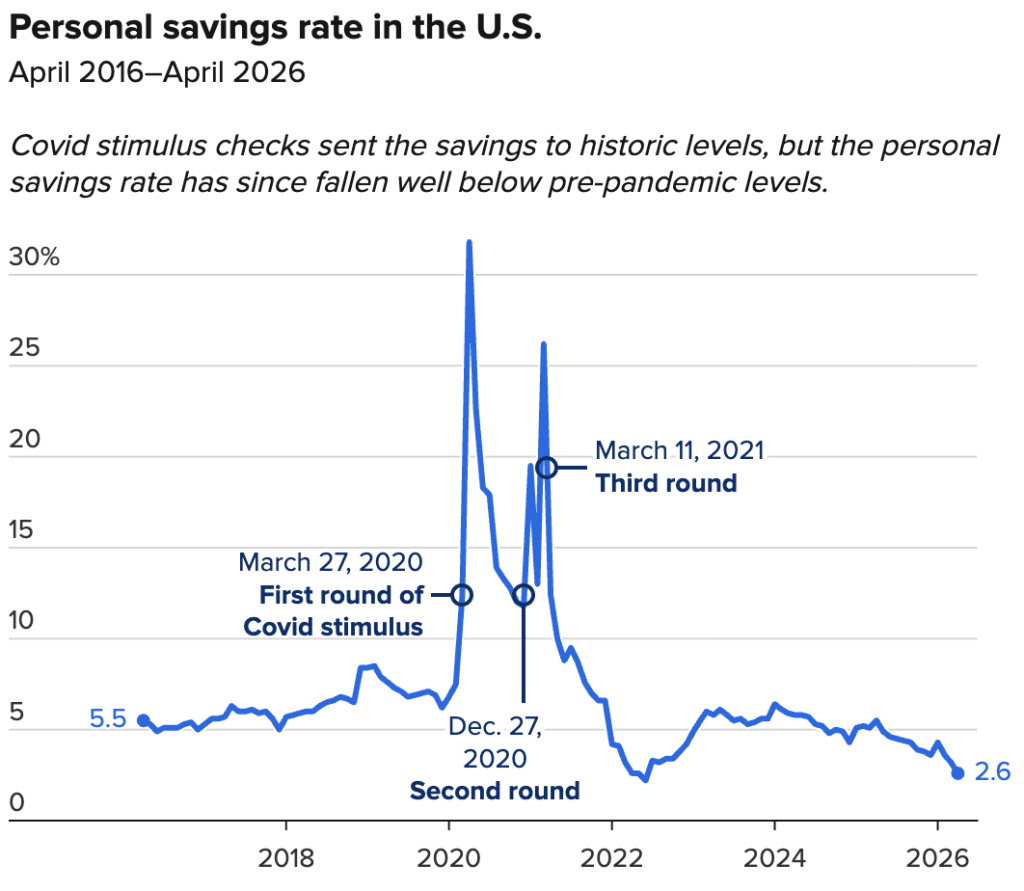

The jump in delinquencies is happening at the same time Americans are saving less money and leaning more on credit to manage monthly expenses. The US personal savings rate fell to 2.6% in April, according to Bureau of Economic Analysis data released Thursday. This is the lowest level since 2022 and down from 5.8% a year ago. Heather Long, chief economist at Navy Federal Credit Union, said,

“I thought 2.6% for April was a typo at first. It is so low. Outside of the revenge spend era of 2022, the personal savings rate has almost never been this low in the past 65 years.”

Also Read: Standard Chartered Sees Ethereum Price at $40,000 Despite ETH Slump

Inflation rose 3.8% in April, while wage growth came in slightly lower at 3.6%. This means incomes are no longer keeping pace with rising prices. Higher fuel, grocery, healthcare, and utility costs have continued to pressure household budgets in recent months.

Consumer spending still increased 0.5% in April. This is even though economists noted much of that rise reflected higher prices rather than stronger demand.

A recent NerdWallet survey found that 37% of Americans expect to rely on credit cards, Buy Now Pay Later services, or loans to cover at least part of their expenses this month.

There are also broader signs of strain appearing across household finances. Credit card delinquencies have been rising. More workers are taking loans or hardship withdrawals from retirement accounts, according to recent Fidelity data.

Economists have increasingly warned that lower- and middle-income households are feeling the impact of elevated living costs more acutely. This comes as spending in other parts of the economy remains relatively stable.

Also Read: Dell Stock Continues 57% Rally Since Trump Endorsement

Written by Sahana Kiran

Sahana Kiran has been covering financial markets since 2019, with a focus on cryptocurrencies, fintech, and the geopolitical events shaping them. She previously reported for AmbCrypto and Watcher Guru, and now writes for BlockNow.