Bitcoin

August 6, 2026

OpenAI Files to Dismiss Apple Lawsuit, Microsoft AI Revenue Tied 70% to ChatGPT Maker

The petrodollar refers to the arrangement where oil is priced and traded globally in US dollars, forcing countries to hold dollar reserves to purchase energy. This system emerged in 1974 when Saudi Arabia agreed to price oil exclusively in dollars in exchange for US military protection, creating permanent global demand for the US currency.

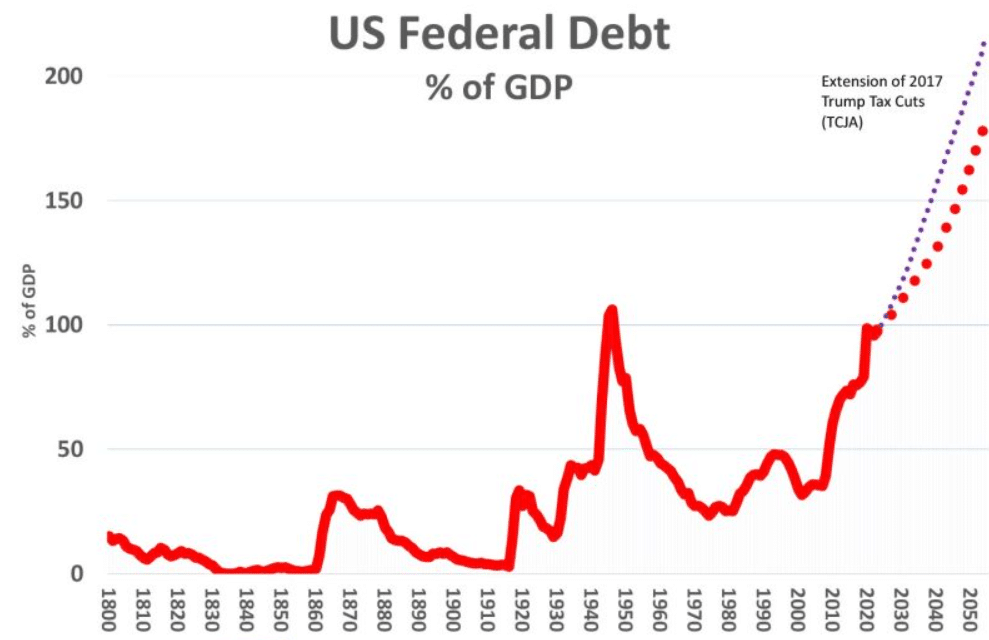

Oil-exporting countries accumulate billions in dollars daily and reinvest them into US Treasury bonds, a process called petrodollar recycling. This mechanism helps finance the $39 trillion US debt while keeping borrowing costs artificially lower. Right now, the petrodollar faces its biggest test in decades as the Iran conflict disrupts flows through the Strait of Hormuz and BRICS nations explore alternatives.

Also Read: Iran Proposes Hormuz Deal to US but Delays Nuclear Talks Until After War

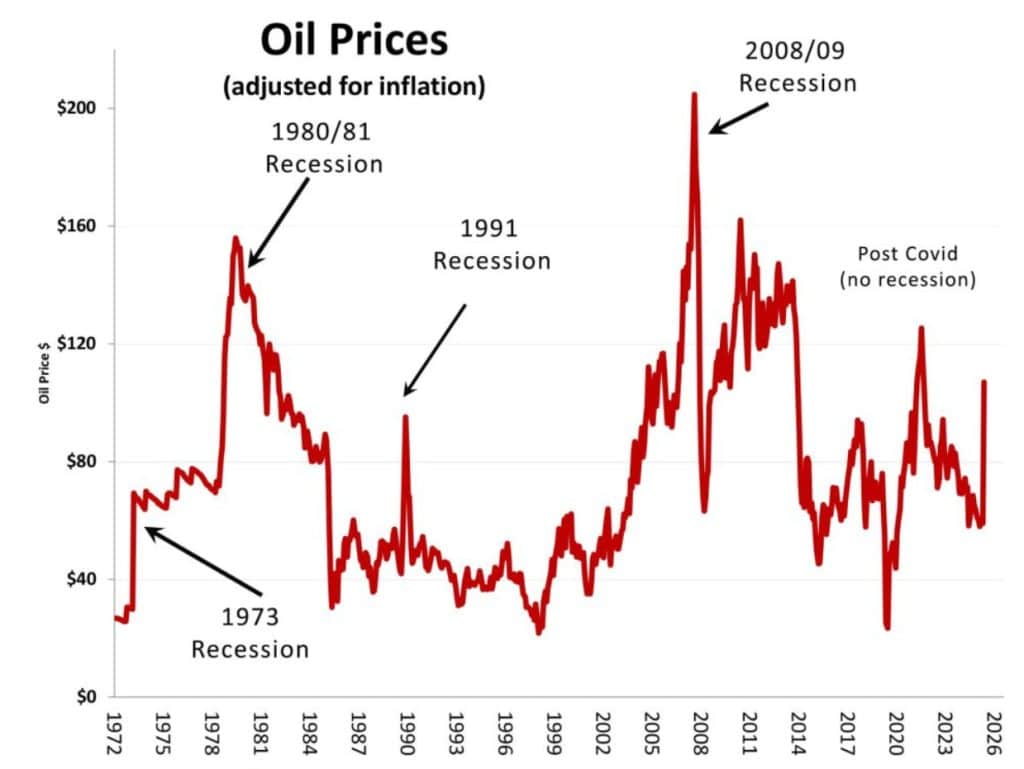

In 1971, President Nixon abandoned the gold standard after Vietnam War spending drove inflation higher. The 1973 oil embargo caused the oil price to quadruple, transferring unprecedented wealth to OPEC nations. The US formalized the petrodollar arrangement in 1974, replacing gold backing with energy backing and making the US dollar mandatory for all global oil purchases.

Every nation needing oil must first obtain US dollars to complete transactions. Oil exporters then recycle surplus revenues into US Treasury securities, creating a closed loop. Edward Fishman, director of the Center for Geoeconomics at the Council on Foreign Relations, explains the system’s importance:

“When you think about the dollar as the world’s dominant currency, the petrodollar is right at the heart of that.”

This recycling keeps US interest rates lower than they would be otherwise, allowing persistent trade deficits without currency depreciation. The continuous demand supports the dollar’s status as the world reserve currency, giving the US what French officials called “exorbitant privilege” in the 1960s.

Also Read: Oil Price: Goldman Raises Brent to $90 as Record Inventory Draws Accelerate

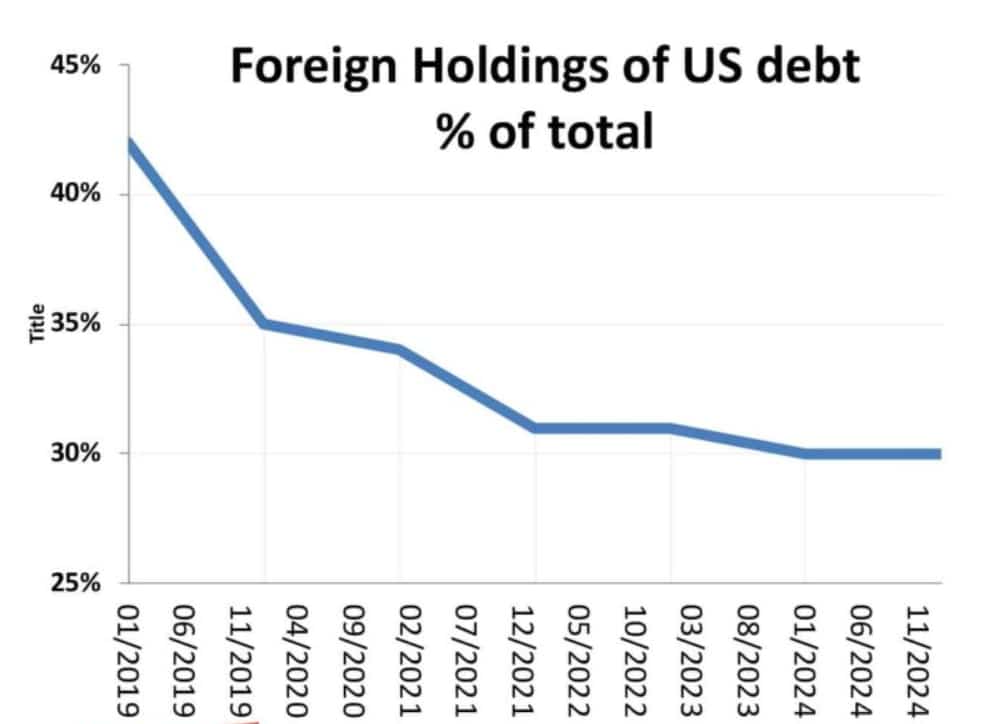

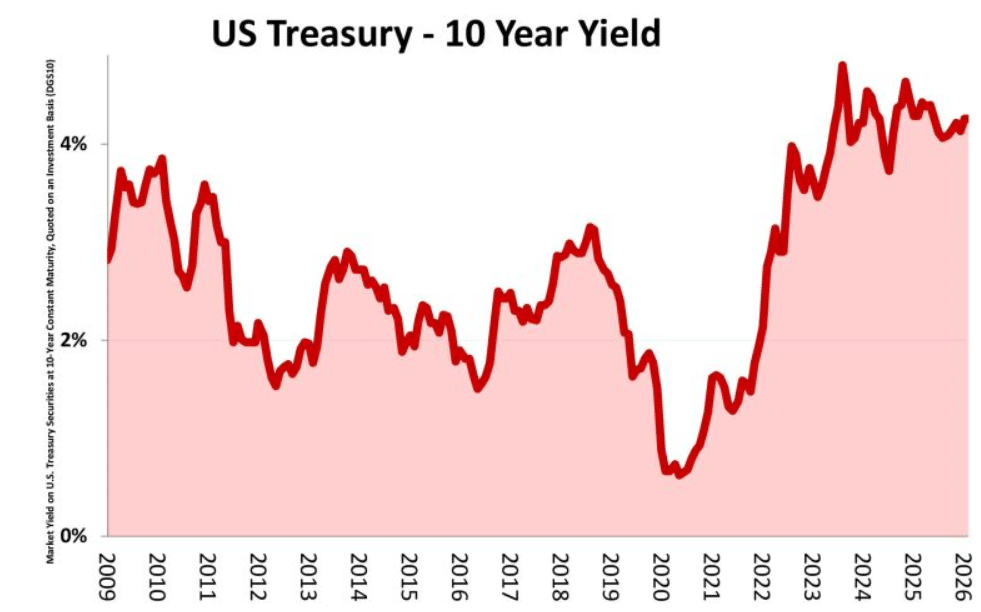

The Saudi agreement to exclusively price oil in dollars ended in 2024. Foreign holdings of US Treasuries have fallen to a 16-year low under $3 trillion, down from over 40% of total US debt in the early 2010s to just 30% now. The war in the Gulf has hit production, forcing Gulf states to step back from buying Treasuries and in some cases actively sell them.

With federal debt requiring more financing, a 1% rise in bond yields could increase debt interest payments by $300 billion annually. US Treasury yields have already risen significantly since 2022.

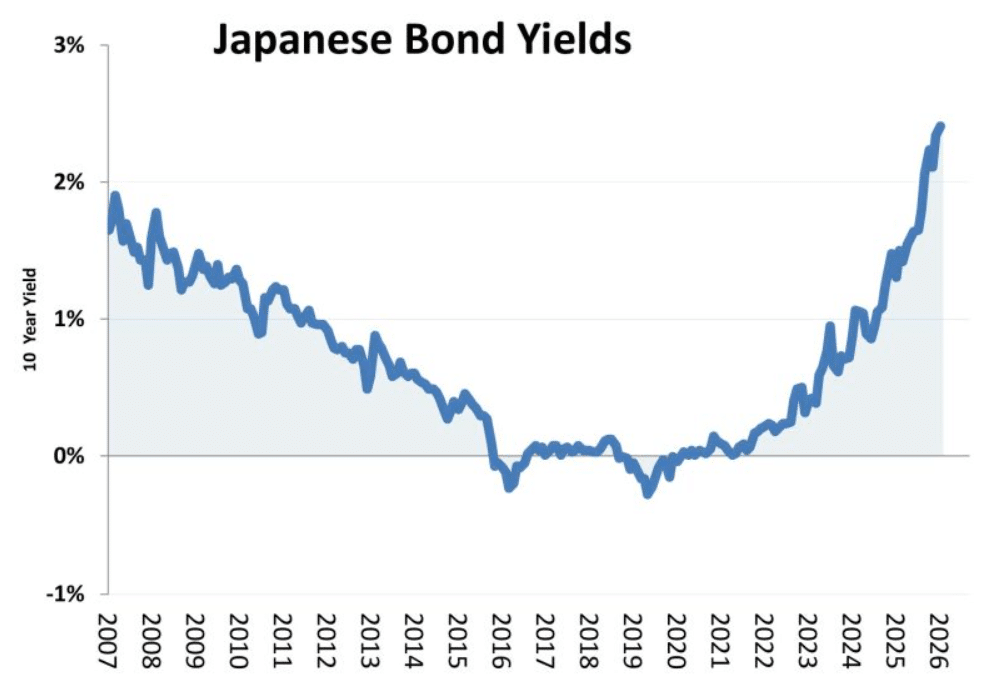

Japan, the biggest holder of US Treasury debt at $1.2 trillion, faces changing conditions. Rising bond yields in Japan are weakening the yen carry trade that previously supported Treasury demand. With public debt at 240% of GDP, Japan has domestic priorities.

For many years, ultra-low interest rates in Japan encouraged investors to borrow cheaply in yen and use those funds to buy higher-yielding US Treasuries. This yen carry trade supported consistent demand for the US dollar and helped finance American debt. As borrowing costs rise in Japan, investors are less willing to maintain these positions and more likely to bring money back home, creating an incentive to sell US Treasuries.

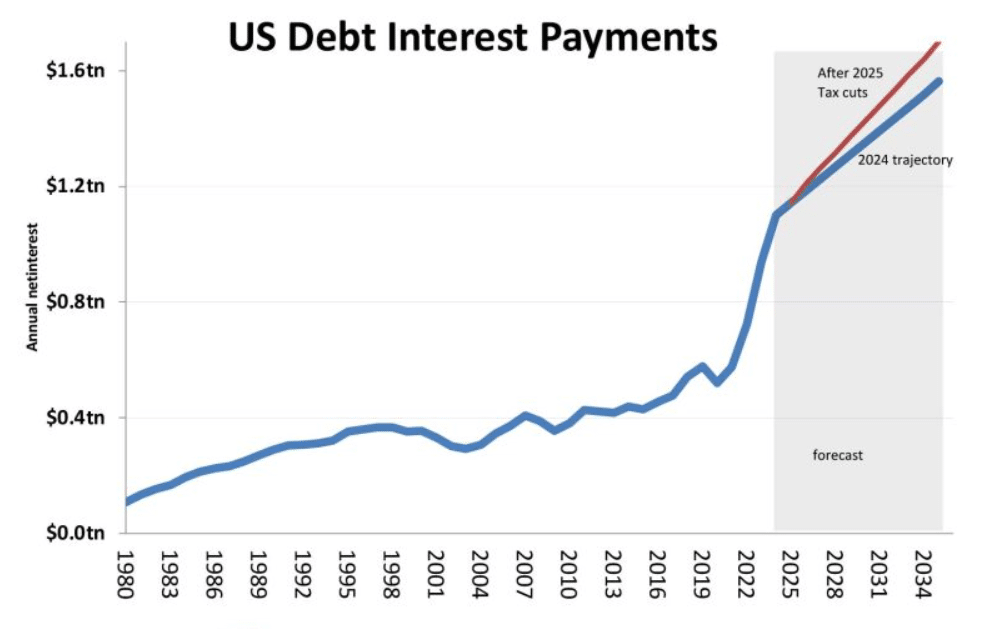

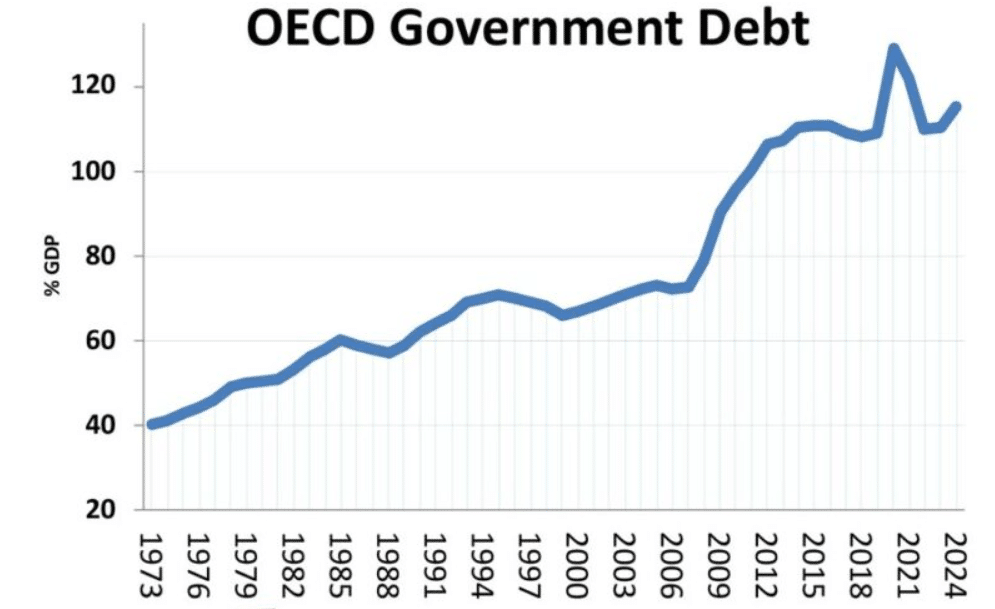

The timing could not be worse for the US. Even before potential higher bond yields materialize, US debt interest payments are already set to increase dramatically because of higher borrowing levels. Debt interest payments have been climbing steadily and are projected to reach over $1.6 trillion annually in the coming years. That represents funds that cannot be spent on Medicare, infrastructure, or other domestic programs.

Public sector debt is rising across the world, driven by slowing growth and ageing populations. With ageing populations, governments must spend more on pensions while receiving less in tax revenue. This global trend means more countries are focused on financing their own debt rather than purchasing US Treasuries, further reducing the pool of foreign buyers that the petrodollar system once guaranteed.

Ken Rogoff, Harvard economist and former IMF chief economist, describes the current moment’s significance:

“This is really bigger than Liberation Day.”

Iran currently sells oil priced in yuan, and the Strait of Hormuz carries more than a fifth of global oil, roughly 21 million barrels daily worth around $530 billion per year. Iran is seeking to charge tolls in yuan or crypto for passage through the strait. Safiya Ghori-Ahmad, senior director with APCO Worldwide, warns of the consequences:

“What that leads to over time is diversification away from the dollar.”

BRICS nations are exploring alternatives to dollar-based trade. China has cut US Treasury holdings from $1.3 trillion in 2013 to $682 billion by November 2025. The dollar’s share of global reserves has declined from 71% to 56.3% since 2008, while central banks have purchased over 1,000 metric tons of gold annually for three consecutive years.

The green energy transition threatens long-term oil demand and structural support for the petrodollar. Christine Lagarde, European Central Bank President, noted in May 2025 that investors “unsettled by unpredictable US economic strategies” are reducing dollar exposure, creating a “global euro moment” opportunity.

Despite pressures, the petroyuan represents only 5% of global oil trade. The yuan is not fully convertible, limiting its use. US financial markets remain more liquid, and entrenched systems still favour the US dollar. The US Treasury market offers unparalleled depth for sovereign funds.

Also Read: X Money Launch: 6% Savings Crushes Banks as Musk Opens to 600M Users

Since the Iran crisis, the dollar has strengthened temporarily as the US is now a net oil exporter. However, long-term pressures are mounting. The US Treasury is no longer the unquestioned safe haven, especially with the US as a belligerent in the current conflict.

The fate of the petrodollar will depend on how quickly alternative currencies replace dollar-based oil trade. In the short term, disruption is more likely than immediate collapse of dollar dominance.

Written by Vladimir Popescu

Vladimir Popescu leads editorial coverage at BlockNow, with over 8 years in financial and tech journalism. He previously held editorial leadership roles at Watcher Guru and Windows Report, and has been cited by Forbes for his crypto market coverage.