Markets

July 27, 2026

Robinhood Stock Falls Despite Crypto.com’s Prediction Markets Partnership Talks & Bernstein’s $160 Target

Key Takeaways

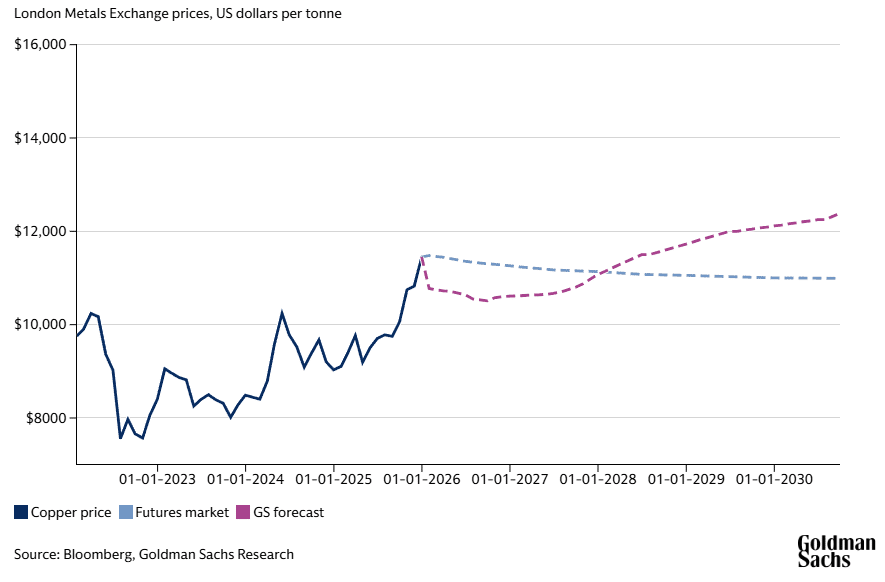

Copper price is sitting near its all-time closing high right now, and the Goldman Sachs revision that just dropped explains a large part of why. The bank had originally forecast a 60,000-tonne deficit in the copper market outside the US this year. That figure has now been revised up to 640,000 tonnes, a tenfold jump in a matter of weeks. Aluminum has hit a four-year high at the same time, with some analysts calling for prices above $4,000 per tonne, which would be all-time high territory. The Iran war, now in its fourth month, is creating what HSBC chief economist Paul Bloxham has been calling a “super-squeeze” on industrial metals, and it is hitting supply from several independent directions at once.

Also Read: Iran Shut Hormuz and Hit the US 5th Fleet as Trump Claimed He Controls the Strait

The copper price squeeze playing out right now is not the result of one disruption. It is several independent supply problems arriving simultaneously, each serious enough on its own, and collectively pushing the market into territory that analysts are struggling to price correctly. The sulphur shortage, the mine disruptions, and the aluminum chokepoint are three separate mechanisms removing supply from the market at the same time, against a demand backdrop that is not slowing down.

Sulphur is a byproduct of oil refining. When refining activity drops, as it has since disruptions to the Strait of Hormuz began, sulphur output drops with it. Sulphuric acid is a critical reagent used in copper and nickel mining operations, and without adequate supply, mines cannot run at full capacity. The price of sulphur has more than doubled since the conflict escalated.

Wood Mackenzie estimates the disruption could remove as much as 125,000 tonnes of copper production in the Democratic Republic of Congo. Morgan Stanley analyst Amy Gower has put a further 200,000 tonnes of Chilean copper at risk, partly from sulphur disruptions and also from China’s ban on sulphuric acid exports. That is 325,000 tonnes of potential supply loss from a single input commodity that almost nobody was watching.

Amy Gower stated:

“It feels like copper supply is getting harder to deliver.”

She added that long recovery times at mines that have experienced disruption are also contributing to the tightness.

The copper market was already expected to be in deficit this year before any of the Middle East disruptions. Goldman’s revised 640,000-tonne deficit number also reflects mine supply problems at Grasberg in Indonesia and at Kamoa-Kakula in the DR Congo, two of the largest copper-producing operations in the world.

Mining executives have said the shortfall has been building for years. Cobus Loots, chief executive of Pan African Resources, pointed to a long period of underinvestment:

“Since the early 2000s, investors have been pushing mining companies to be more capital-disciplined, which is a great thing, but it also means potentially underspending and underinvesting in new supplies. Now there has to be some level of catch-up.”

UBS has gone even further, forecasting copper hitting $15,000 per tonne by the end of March 2027.

Also Read: Social Security Electronic Benefits Update: Paper Checks End for 280,000 Americans in 2026

The aluminum price 2026 story is running in parallel with copper and is in some ways more acute right now. The Middle East accounts for nearly 10% of global refined aluminum production, and that supply has been cut off from global consumers by shipping disruption through the Strait of Hormuz. More than 5 million tonnes of aluminum passed through the strait last year, going to around 70 countries across Asia, Europe, and North America.

Major producers Alba and EGA curbed output after Iranian strikes damaged their infrastructure. Qatalum also announced production and delivery stoppages. Force majeure has been declared at two Gulf producers. Cash aluminum contracts were as much as $116.50 per tonne more expensive than three-month futures on June 2, the biggest such premium since 2007, and aluminum was up more than 25% year-to-date at the time of writing.

On top of this, Europe is taking hits from multiple sides, with Russian supply already gone, domestic smelters closed due to high energy costs, and the imminent loss of the Mozal smelter in Mozambique. Citi has said the aluminum price 2026 supply-demand setup is the most bullish in at least half a century.

Data centers use copper for wiring and aluminum for server racks. The AI boom is driving demand for both right now, at exactly the moment supply is being removed from multiple directions. High fuel prices from the Iran war are also pushing countries to accelerate energy transition investments, which adds further medium-term demand for copper and aluminum on top of an already stressed market.

Paul Bloxham at HSBC, who has been using the term “super-squeeze” since the aftermath of Russia’s invasion of Ukraine in 2022, said this cycle is fundamentally different from what came before:

“This is very different to earlier supercycles because it is driven by supply disruptions, not strong demand. This is going to be a positive story for copper, nickel, aluminium, for products that are a big part of the energy transition.”

He also noted the same supply constraints represent a “huge negative supply shock to the global economy.”

Jean-Sébastien Pelland, executive director at Eland Cables, which produces copper cables for offshore wind farms and oil rigs, said demand destruction is simply not visible in his market:

“People are not going to stop buying cables for renewables energy any time soon.”

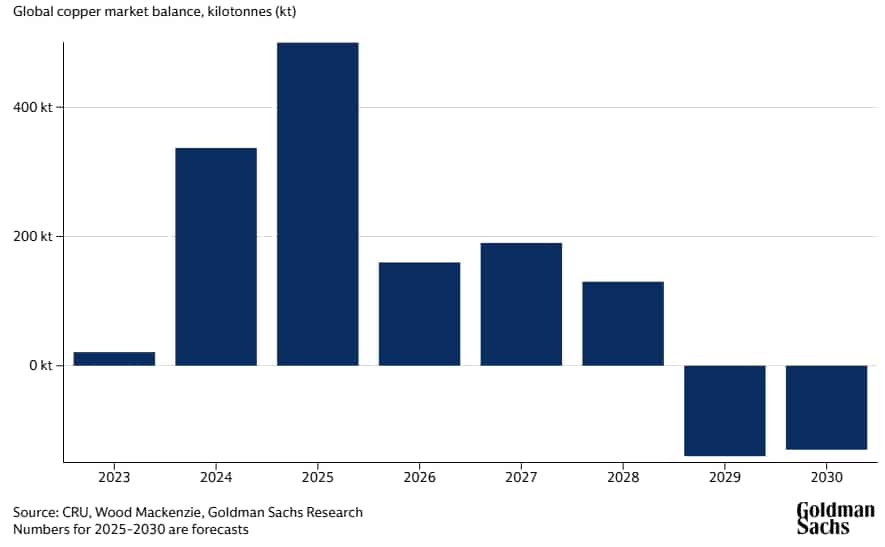

This is where the copper price forecast picture consolidates into something concrete. Goldman Sachs has raised its year-end copper price forecast by more than 10% to $13,735 per tonne, driven by the revised 640,000-tonne deficit and the mine supply disruptions at Grasberg and Kamoa-Kakula. The latest Goldman Sachs copper demand projections also show the market moving into sustained deficit from 2029 onwards, which will push prices structurally higher and begin incentivizing new supply development through mine life extensions and increased scrap use.

UBS is more aggressive than Goldman on the copper price forecast, targeting $15,000 per tonne by the end of March 2027. Citi has put $4,000 per tonne on the table for aluminum in a bull case scenario, and described current conditions as a clear shift from supply risk to realized disruption. Morgan Stanley’s Gower has been among the more cautious voices but still flagged 200,000 tonnes of Chilean supply at risk, which is a significant number on its own.

Also Read: Gold Erases 2026 Gains Despite China’s Biggest Purchase Since January 2025

The broader commodity picture, which includes the Iran war oil price feeding into diesel, transportation, fertiliser, plastics, and sulphur simultaneously, is what makes this moment different from isolated supply shocks of the past. Craig Miller, CEO of Valterra Platinum, put it plainly:

“We are going to be in a much tighter supply environment across commodities. The demand for metal is going to continue to grow. And supply has not grown, by any stretch of the imagination, to meet that demand.”

The copper price picture right now is the product of several independent problems arriving at the same time. A war disrupting a critical shipping chokepoint. A sulphur shortage that nobody saw coming. Years of underinvestment in mine supply. And demand from AI and the energy transition that is not going to pause while the market sorts itself out.

Goldman Sachs copper analysts have revised their deficit estimate tenfold in a matter of weeks. UBS sees $15,000 per tonne copper by early 2027. Aluminum is at a four-year high and closing in on all-time high territory. The same Hormuz disruption, the same structural underinvestment, and the same relentless demand growth are pushing the aluminum price 2026 trajectory in the same direction as copper.

What makes this moment different from previous commodity cycles, as Bloxham at HSBC put it, is that the squeeze is coming from the supply side, not from an overheating economy. That means there is no central bank lever to pull to fix it. New mines take years to build. Sulphur supply recovers only when oil refining recovers. And the Iran war oil price impact on operating costs is not going away until the conflict does.

Also Read: BofA CEO Warns Stablecoin Yield Could Drain 35% of All US Bank Deposits

The gap between where supply is and where demand is going is the story. And right now, that gap is getting wider.

Written by Vladimir Popescu

Vladimir Popescu leads editorial coverage at BlockNow, with over 8 years in financial and tech journalism. He previously held editorial leadership roles at Watcher Guru and Windows Report, and has been cited by Forbes for his crypto market coverage.