BRICS

May 20, 2026

Putin-Xi Beijing Summit Comes Days After Trump Visit as China Flexes BRICS Influence

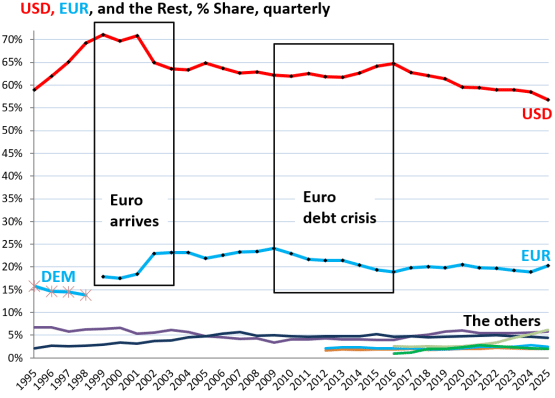

What is de-dollarization? It is not a conspiracy theory but a measurable, documented, IMF-confirmed structural shift in how the world uses money. The US dollar’s share of global foreign exchange reserves has fallen from 71% in 1999 to 56% in 2026, the lowest level since 1994, according to IMF COFER data. That is not a collapse, but it is a 25-year trend that accelerates rather than reverses. What is de-dollarization in practice? Central banks, governments, and trading nations are reducing their dependence on a dollar-dominated system.

They are building alternatives through local currency trade, gold accumulation, and parallel payment infrastructure. The BRICS vs dollar conflict sits at the center of that shift as BRICS nations represent 48.5% of the world’s population and 40% of global GDP. Some 67% of intra-bloc trade already gets settled in local currencies, up from under 20% a decade ago. That is what is de-dollarization looking like in real trade flows. Questions about what is BRICS currency and whether it can challenge the dollar, how the petrodollar decline plays out, and whether the dollar can hold its position define the debate right now.

Also Read: Russia and China Now Settle 95% of Trade Without Dollars as De-Dollarization Completes

Not everyone agrees on how far this goes. CNBC’s analysis of dollar dominance and its challengers captures the split well. “There is no alternative,” Elias Haddad, global head of markets strategy at Brown Brothers Harriman, told CNBC. “All other currencies are nowhere near an environment to replace the dollar.” Even defenders of dollar dominance acknowledge the structural downtrend has “further to go,” though. Fortune’s coverage of the petroyuan and dollar erosion makes a similar point: the petrodollar system is under real pressure, even if no single currency stands ready to replace the dollar. The petrodollar decline, the BRICS vs dollar infrastructure, and the BRICS Unit all form part of the same broader story.

What is de-dollarization at its most basic and why does it matter right now? It is the process by which the US dollar loses its role as the world’s dominant reserve currency. It also loses its place as the primary trade settlement currency and its status as the default unit of account in global finance. The IMF, the World Gold Council, and the Bank for International Settlements all confirm this in real data. The dollar’s reserve share dropped from 72% in 2001 to 56%, a 16-percentage-point decline over roughly two decades, and the pace picked up sharply after 2022.

What is de-dollarization driven by right now? Well, the weaponization of dollar-based financial infrastructure through sanctions gave dozens of countries a practical reason to build alternatives. The United States regularly spends far more than it collects in revenue, which raises structural questions about the long-term value of holding dollar-denominated assets. The BRICS vs dollar infrastructure also gets built in parallel, making alternatives increasingly viable. The incentives to hold dollars weaken while the alternatives improve. Central banks responded in part by buying gold. The data on gold now making up 24% of central bank reserves sits alongside the dollar’s reserve decline as part of the same structural shift. Both trends accelerate together, and that is what is de-dollarization at the macro level.

To understand what is de-dollarization and why it matters, you have to understand how dollar dominance got built. In July 1944, 44 Allied nations gathered at Bretton Woods, New Hampshire. They agreed to peg their currencies to the US dollar, which itself pegged to gold at $35 per ounce. The dollar became the anchor of the entire global monetary system. It was the currency in which international trade settled, debts got denominated, and reserves got held. Every central bank on earth needed dollars to function.

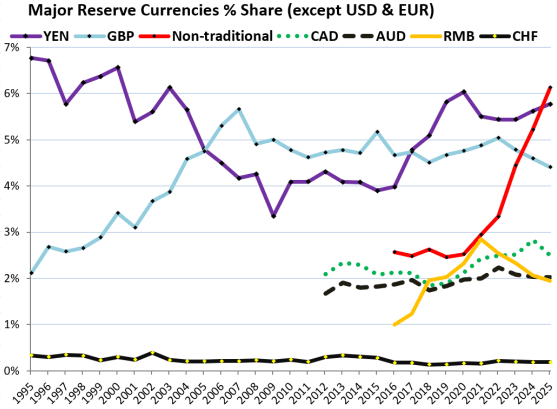

The Bretton Woods system collapsed in 1971 when President Nixon ended dollar-gold convertibility, but the dollar’s reserve currency status survived and actually strengthened through what came next: the petrodollar system. What is de-dollarization in historical context? It is the story of how that 1944 arrangement gets slowly renegotiated. Not at a conference table, but through bilateral deals, payment system choices, and central bank decisions made every day. De-dollarization explained historically is, at its core, the story of that renegotiation. Understanding the petrodollar decline starts with understanding what made it so powerful in the first place and how that power gets dismantled. And what replaced the dollar’s share is also telling. It was not the yuan or the euro that gained share, but dozens of smaller “non-traditional” reserve currencies. Their combined share more than doubled after 2021.

The petrodollar decline connects directly to what is de-dollarization in practice. In 1974, Secretary of State Henry Kissinger and Saudi Crown Prince Fahd struck a framework agreement. Saudi Arabia would price oil exclusively in US dollars and recycle surplus petrodollars into US Treasury securities. Washington provided military protection for the Kingdom’s oil fields in return. By 1975, every OPEC member agreed to dollar-denominated pricing. The arrangement gave the US a structural advantage that lasted five decades. Persistent trade and budget deficits could run without triggering currency crises because global oil demand automatically created global dollar demand. That is why analysts consider the petrodollar system the structural foundation of American financial hegemony. The petrodollar decline, then, is not just an energy story but one about American power.

As Fortune reported, Deutsche Bank noted that Saudi Arabia had been selling more than four times as much oil to China as to the US, with 85% of Middle East crude flowing to Asia. Saudi Arabia chose not to formally renew the petrodollar agreement in 2024. It also joined Project mBridge, a cross-border central bank digital currency platform that runs independently of SWIFT and dollar correspondent banking. MBridge was developed with the central banks of China, the UAE, Thailand, and Hong Kong and the petrodollar decline accelerated the moment these institutions started building together.

What is de-dollarization through the oil market? Indian refiners settle approximately 60 million barrels per month of Russian crude in yuan and UAE dirhams, according to Bloomberg. Russia prefers yuan because it converts to rubles in a single step and enables direct purchases of Chinese goods. The broader context, including the Iran strikes on US bases and the UAE Hormuz pipeline, shows how quickly these dynamics escalate beyond finance.

The turning point in the de-dollarization story came in February 2022 when Western governments froze $300 billion in Russian central bank reserves following the invasion of Ukraine. A very clear message went to every sovereign wealth manager and central bank on earth: dollar reserves in Western institutions can get seized. The structural response came fairly quickly and central banks began buying gold at record annual rates.

Bilateral trade deals have increasingly begun bypassing SWIFT. The alternative financial infrastructure quietly developed by BRICS since around 2014 has started to receive far more urgency and attention. The freezing of assets transformed what was once a theoretical risk into a proven reality, offering a concrete answer to what de-dollarization actually means: it occurs when confidence in the US dollar as a safe store of reserves begins to erode. This shift has also accelerated the gradual decline of the petrodollar system. Energy-importing countries have started to explore non-dollar settlement for oil transactions, seeking alternatives before they find themselves exposed to the same vulnerabilities experienced by Russia.

At the Saint Petersburg International Economic Forum, Russian President Vladimir Putin spoke directly about what that freeze did to global confidence in the dollar:

“Sanctions and basically the theft of Russia’s international reserves has had an irreversible effect on the positions of the world currencies, namely the US dollar and euro.”

He also framed it as a warning to every country still watching:

“The weapon that the previous U.S. administration attempted to use turned out to be a catastrophic strategic mistake. Now everyone is asking themselves: what will happen to our reserves?”

Russia’s own numbers tell the story directly as it now conducts approximately 65% of its export transactions in rubles. That shift happened under sanctions pressure, but it also demonstrated that non-dollar trade infrastructure works at scale. Central bank gold purchases surged after 2022 and have not slowed down and the World Gold Council reported net purchases of 863 tonnes for full-year 2025.

The actual total is estimated to exceed 1,100 tonnes and China stopped disclosing its gold purchases in 2024, which accounts for the gap. Gold’s share of global reserves rose from 13% in 2017 to around 30% in 2025 and BRICS+ nations now hold an estimated 6,000 tonnes collectively, representing 17.4% of global central bank gold reserves, up from 11.2% in 2019. The World Gold Council projects another 750 to 850 tonnes of official purchases in 2026. What is de-dollarization if not this kind of long-term structural hedging? The Russia Bitcoin Property Bill also fits this picture, as Russia moves to legitimize non-dollar asset classes at the legislative level.

The BRICS vs dollar conflict does not play out through declarations, but through payment rails, swap lines, and settlement infrastructure. China’s CIPS payment system, the closest operational SWIFT alternative right now, processed $25 trillion in annual volume in 2025, up 43% year on year. Even more, Russia and China settle around 90% of their bilateral trade in rubles and yuan. That is the BRICS vs dollar dynamic playing out at the bilateral level. The BRICS bloc itself covers Brazil, Russia, India, China, South Africa, Saudi Arabia, the UAE, Iran, Egypt, Ethiopia, and Indonesia, which represents roughly 45% of the world’s population and over 35% of global GDP by purchasing power parity. The addition of Saudi Arabia and the UAE gave the BRICS vs dollar dynamic a direct foothold in global oil pricing and OPEC.

The UAE joining BRICS and participating in mBridge while deepening energy ties with China captures the BRICS vs dollar story in a single relationship. Xi Jinping’s meeting with UAE Crown Prince Sheikh Khaled in Beijing focused on expanding energy cooperation. It is one of many such bilateral moments that add up to a structural realignment rather than a symbolic gesture.

At the BRICS Summit in Kazan, Putin put the broader BRICS vs dollar case plainly:

“The dollar is being used as a weapon. We really see that this is so. I think that this is a big mistake by those who do this.”

India keeps distance from the maximalist reading of what the BRICS vs dollar conflict means. India’s External Affairs Minister S. Jaishankar made the country’s position clear:

“I don’t think there’s any policy on our part to replace the dollar. The dollar as the reserve currency is the source of global economic stability, and right now what we want in the world is more economic stability, not less.”

The official BRICS position amounts to a “strategy of practical gradualism,” as the BRICS Council described in 2026. The goal is building enough parallel infrastructure so that the dollar becomes one settlement option among several rather than the only viable one. That is also what makes the BRICS vs dollar shift durable: it requires no confrontation to succeed, only alternatives. The BRICS vs dollar story is not about aggression. It is about optionality. The petrodollar decline is one of those alternatives becoming real, transaction by transaction.

Also Read: The Petrodollar System: Why Oil Traders Can’t Escape the US Dollar

The question of what is BRICS currency comes up constantly in the de-dollarization debate, and the answer is simpler than most headlines suggest. There is no single BRICS currency, and no serious plans exist to create one anytime soon. Russia confirmed in early 2026 that talks on a unified currency “have not taken place and are not taking place now.” What does exist is the BRICS Unit, a cross-border trade settlement instrument launched as a pilot in late 2025, backed 40% by gold and 60% by a basket of BRICS member currencies. It is not a coin, not a banknote, and not something central banks hold as a reserve asset.

So when people ask what is BRICS currency and whether it threatens the dollar, the honest answer is simple: not directly, and not yet. What it does is reduce the number of transactions that require dollars as an intermediary. That is exactly what de-dollarization explained at a structural level looks like. The BRICS Unit is not a reserve currency but a building block. The BRICS Summit in New Delhi will put interoperability of BRICS payment systems on the formal agenda and the outcome will signal whether cross-border settlement advances from pilot to operational scale.

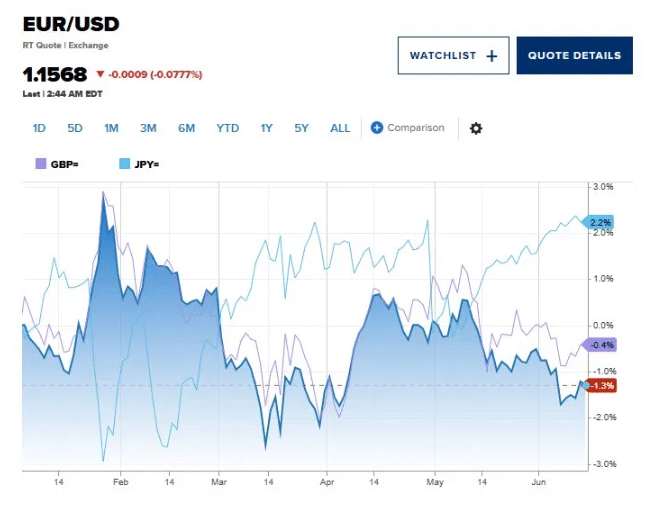

What is de-dollarization in raw data? The dollar is not dying and the BIS 2025 Triennial Central Bank Survey found the US dollar on one side of 89% of all foreign exchange transactions in April 2025. That is actually up from 88.4% in 2022. Global FX trading reached $9.6 trillion per day. The yuan’s share rose to 8.5%, which is meaningful growth but still a fraction of dollar volumes. Foreign central banks held $7.46 trillion in USD-denominated assets in Q4 2025, according to IMF data. That figure is essentially flat since 2014. The share falls not because dollar holdings get dumped. Holdings in dozens of other smaller currencies simply grow faster. That is relative decline, not absolute collapse, and the distinction matters.

Currency markets tell a similar story. The dollar softened against the euro, sterling, and yen through much of 2026, not collapsing but also not recovering the ground it lost, which is also what a structural erosion looks like in practice.

Franklin Templeton’s fixed income CIO Sonal Desai pushed back against the more dramatic predictions in 2026:

“Oil exporters have a strong self-interest in getting paid in USD, because of what dollars represent: access to the deepest, most liquid capital markets in the world, backed by an institutional and legal framework that protects property rights and enforces contracts, supported by a strong, dynamic, and innovative economy.”

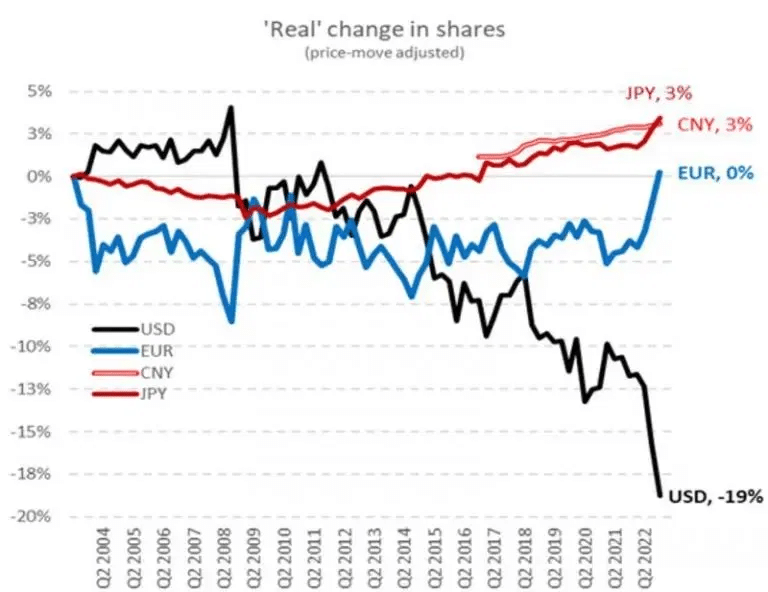

Price-adjusted data makes the picture even clearer. Once you strip out currency valuation movements, the dollar lost 19% of its real reserve share between 2004 and 2022, while the yuan and yen each gained roughly 3%. The nominal figures understate the actual shift.

The fiscal picture adds another layer. The US government regularly spends far more than it collects in revenue, running deficits that rely on foreign demand for US Treasuries to remain financeable. Brown Brothers Harriman’s Haddad told CNBC that fading US fiscal credibility gives the structural downtrend in dollar reserve share further room to run. Pressure on the Federal Reserve adds to that. De-dollarization ultimately is what happens when the incentive to hold dollars weakens faster than the alternatives improve. Right now both of those things happen simultaneously, and what is de-dollarization if not exactly that convergence in action.

What is BRICS currency doing to the petrodollar decline in practice, and what does any of this mean for ordinary Americans? The dollar’s reserve currency status allowed the United States to run persistent trade and budget deficits for decades. No other country in the same position could have done so without triggering currency crises. Foreign central banks buying US Treasuries effectively subsidized American borrowing costs. If that demand declines structurally, and the IMF data suggest it already does, US borrowing costs go up.

The dollar’s purchasing power weakens and import prices for American consumers rise and the petrodollar decline removes one of the key structural sources of dollar demand. When the world no longer needs to hold dollars specifically to purchase oil, that automatic demand disappears. For Americans watching their retirement savings, the Social Security Trust Fund depletion timeline connects directly to the same fiscal pressures that drive dollar reserve outflows and the latest IRS tax refund data reflects how those pressures show up in household finances.

What is de-dollarization from Washington’s perspective, and why does it matter for Americans specifically? It is the slow erosion of financial leverage. The more countries build infrastructure outside SWIFT and outside dollar settlement, the less effective financial exclusion becomes as a tool of foreign policy. The petrodollar decline also narrows Washington’s policy toolkit. Trump threatened 100% tariffs on BRICS nations pursuing this agenda. Brad Setser of the Council on Foreign Relations noted that this creates a real paradox. Coercing countries through tariff threats could well accelerate the very shift Washington tries to stop.

At SPIEF 2026, Putin described the dynamic from the other side:

“All countries, without exception, now understand that just as Russia can instantaneously lose access to their legitimate assets denominated in the US dollar or euro, they can also lose access to the Western financial and payment infrastructure.”

Also Read: India Expands e-Rupee Pilots as Over 40 Countries Engage With BRICS Payment Alternatives

What is de-dollarization at its most fundamental? It is the slow dismantling of a system that never got designed to last forever. The dollar is not getting replaced but the architecture that kept it dominant takes hits piece by piece and the petrodollar decline continues. The BRICS vs dollar infrastructure expands and the margin shrinks. Whether erosion becomes exodus is the question the next decade will answer. Not in a single summit or crisis, but in thousands of individual trade and reserve decisions that governments make every day.

1. Can the Chinese yuan replace the US dollar?

Not anytime soon. The yuan held just 2% of global reserves in 2025 and China maintains capital controls that limit free convertibility, a basic prerequisite for any reserve currency. China’s CIPS system processed $25 trillion in 2025 and the yuan’s share of global trade is growing, but the gap between that and replacing the dollar is enormous. BRICS is currency building a parallel infrastructure, not a dollar substitute.

2. Why did Saudi Arabia stop pricing oil in dollars?

Saudi Arabia did not formally renew the petrodollar agreement in 2024, partly because the trade reality had already shifted. It now sells more than four times as much oil to China as to the US. Some 85% of Middle East crude goes to Asia. Pricing oil exclusively in dollars made commercial sense when the US was the primary buyer. That is no longer the case. The petrodollar decline is the result of that commercial logic, not a political statement. It is also why energy-importing nations started building non-dollar settlement infrastructure.

3. Will the dollar remain world’s reserve currency?

The dollar will almost certainly remain the world’s reserve currency for decades to come. De-dollarization explained through historical precedent suggests transitions take 30 or more years. The British pound took roughly 30 years to move from dominant reserve currency to secondary status, and the dollar starts from a far stronger position. It still sits on one side of 89% of all FX trades, and no alternative comes close to matching its liquidity or the depth of US capital markets. What changes is the margin. The dollar’s share keeps falling, its leverage as a sanctions tool weakens, and the cost of running large deficits slowly rises. What is de-dollarization doing to that long-term picture? It is making the margin smaller, year by year.