Markets

July 26, 2026

Meta Q2 Earnings Spotlight Shifting Monetization Strategies for Mark Zuckerberg

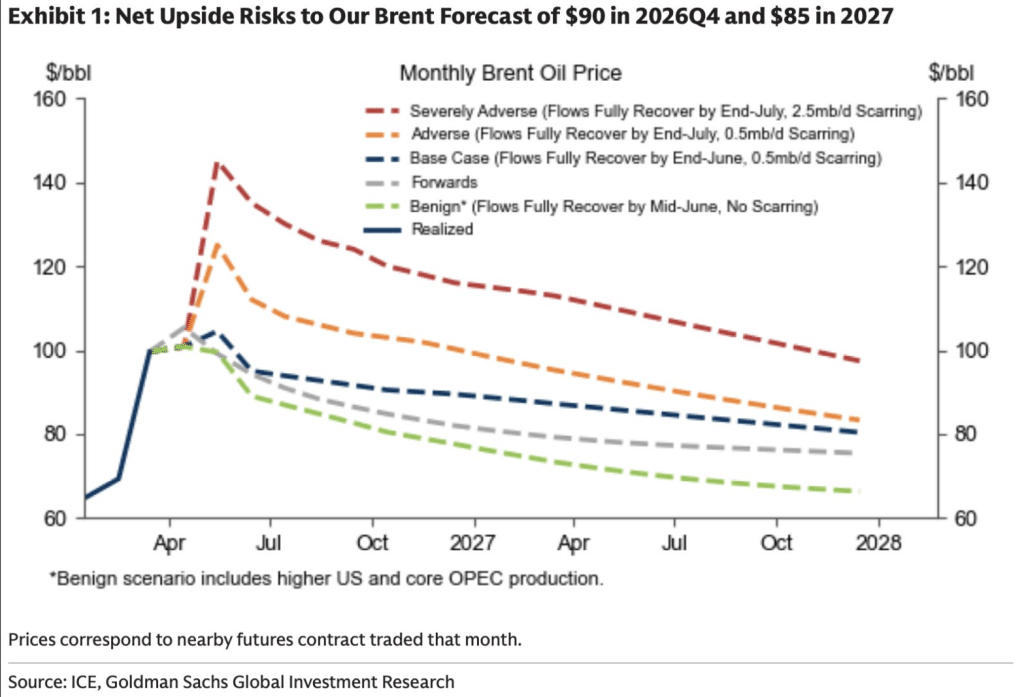

Oil price is sitting at a crossroads that Goldman Sachs has now mapped out in uncomfortable detail. Brent crude oil crossed $110 a barrel and is holding there, gas prices in the US have hit their highest level since 2022, and the Iran war shows no sign of ending fast enough to prevent lasting damage to global supply. Goldman Sachs ran the numbers on every possible outcome and came back with four scenarios, ranging from manageable to genuinely alarming. The oil price forecast covers everything from a soft landing around $71 in Q4 2026 to a $140 peak by June in the worst case, with prices staying near $100 into 2028. The market, by Goldman’s own assessment, has not priced any of this in properly yet.

Also Read: Millions of Americans Could Claim IRS COVID Tax Refund Before July 10 Deadline

The entire Goldman Sachs analysis is built around one question: when does the Strait of Hormuz reopen, and how much permanent damage has been done to Gulf production by then. Each of the four scenarios gives a different answer, and the gap between the best and worst outcomes is roughly $70 per barrel.

In the most optimistic scenario, the Strait gradually restores flows and returns to pre-war levels within about a month, with no lasting scarring to production infrastructure. Goldman estimates Brent crude oil would average around $71 per barrel in Q4 2026. The supply shock under this scenario translates into a roughly 617-million-barrel hit to global commercial oil inventories, with strategic petroleum reserve releases and Russian oil on water offsetting about half the damage. Oil prices would also remain lower for longer as higher US and core OPEC production fills some of the gap.

Goldman’s base case assumes a late-June full resumption of oil flows, by which point Iraq and other producers have already locked in 0.5 mb/d of scarring. Brent reaches $120 under this scenario. Even with the Strait reopened, oil price levels are not expected to return to pre-war territory for years. Goldman sees prices remaining at around $80 per barrel through to the end of 2027, which is the kind of sustained elevation that compounds inflation across every importing economy on the planet.

The adverse scenario sees flows not resuming fully until the end of July, with 0.5 mb/d of scarring still baked in. Brent crude oil would average just over $100 in Q4 under this path. Goldman warns that in scenarios like this one, oil inventories are likely to reach very low levels, triggering non-linear price increases that standard models do not capture well.

This is the scenario that has been getting the most attention. Oil flows do not resume fully until the end of July, and by then a permanent supply reduction of 2.5 mb/d has been caused. Brent hits $140 by June and remains at around $100 a barrel into 2028, which is roughly $30 higher than the pre-war baseline. Goldman stated:

“In the adverse and severely adverse scenarios, oil inventories are likely to reach very low levels, triggering non-linear price increases.”

These scenarios still assume a full Strait reopening within the next eight weeks. If Iran holds out longer, Goldman does not rule out even worse outcomes, with what the bank describes as “increasingly massive impacts on the global economy.”

Also Read: Treasury Yields Hit 9-Month Highs as Bond Market Flips to Rate Hike Pricing

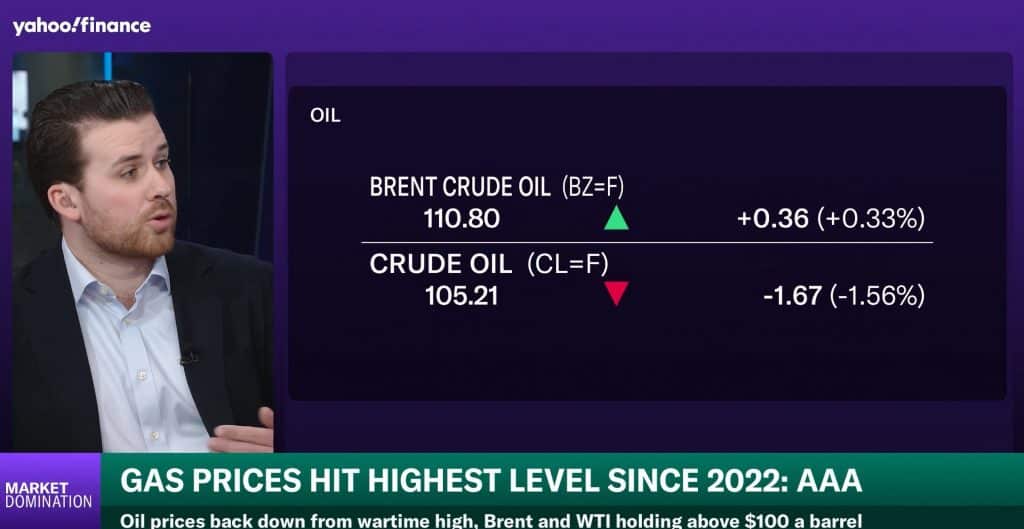

At the time of writing, Brent crude oil is trading at around $110.80 and WTI is at $105.21. Both benchmarks are holding well above $100 even as a two-week ceasefire was announced between the US and Iran. The market is clearly not buying the ceasefire as a meaningful resolution.

The 5-day chart makes the Iran war oil market dynamic pretty visible. WTI surged more than 9% over the week, with the move accelerating mid-week and then pulling back sharply on Thursday as ceasefire headlines hit. Brent and WTI have also been narrowing their usual spread, and any credible threat of US export restrictions would push that gap back out fast.

Also Read: Offshore USD Deposits Hit $14.5T Record, Up 220% Since 2000 Amid De-Dollarization Talk

Trafigura Group Chief Economist Saad Rahim had this to say:

“The scale seems to be something where the market can’t actually get its head around it, so there is the real disconnect between perception and reality right now.”

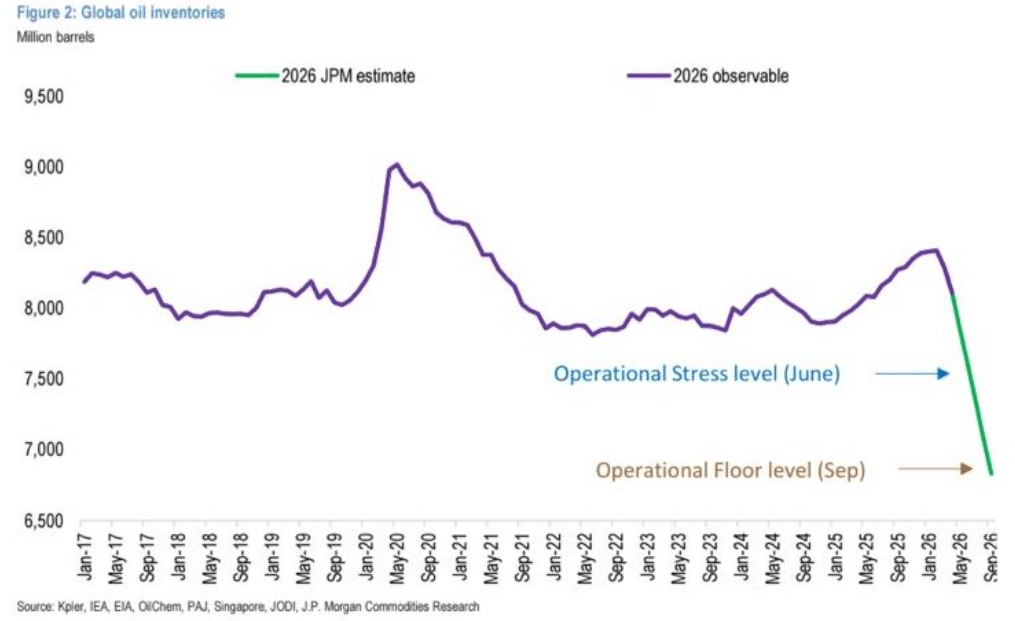

Goldman Sachs oil analysis is not the only institution sounding the alarm on stocks. JPMorgan’s own inventory tracking shows global oil stocks drawing toward operational stress levels by June and potentially hitting the operational floor as early as September. The draw rate in April was running at 11 to 12 million barrels per day, the fastest pace on record since satellite tracking began.

JPMorgan estimates it will take four months for oil exports to fully resume after any reopening. Goldman Sachs projects an even slower recovery for crude production specifically, reaching only about 70% of pre-war output by July and roughly 90% by December, even under a June reopening assumption.

Sankey Research stated:

“We can be sure that the next two months is going to be an ongoing, absolute disaster even if you open the straits tomorrow because it’s just locked in by virtue of tankers, and the tankers are all in the wrong places.”

One part of the Goldman oil price forecast that tends to get lost in the headline numbers is the permanent floor. Regardless of which scenario plays out, the Iran war will permanently add at least $9 to the long-run cost of a barrel of oil, according to Goldman. That translates to about 20 cents per gallon more for gasoline in the US on a persistent basis, and around 5 cents per litre in the EU and UK. Goldman says this premium is expected to hold for years, not just through the acute phase of the disruption.

Also Read: Bitcoin Crosses $81K as ETF Inflows Hit $2.44B in April, Strongest Since October

The five largest prior supply shocks, covering the Iran-Iraq War, Gulf War I, Gulf War II, the Libyan Civil War, and Russia’s invasion of Ukraine, showed that production in affected countries remained more than 40% below pre-shock levels four years later. Goldman flagged that as a direct risk here given that offshore fields dominate the region’s crude production, where ramp-up times run significantly longer than for onshore fields.

Goldman Sachs oil analysts also flagged a tail risk that sits outside the base case but is real enough to be named explicitly. If the Strait of Hormuz remains effectively closed for longer, the bank does not rule out US oil and fuel export restrictions, with the Trump Administration moving to preserve domestic stockpiles at the expense of other importing nations.

The US currently exports around 1.1 mb/d of diesel and 0.7 mb/d of gasoline, flows that many countries have already become structurally dependent on. Cutting those off would compound the Gulf disruption significantly. There is also a built-in contradiction to any ban. The US is a net crude importer by about 2.2 mb/d. Restricting exports would make US shale production less profitable, reduce domestic output, and actually push US gasoline prices higher by squeezing refiner margins.

Also Read: Iran Strikes UAE’s Fujairah Port, Only Hormuz Bypass Burning, Oil Hits $114

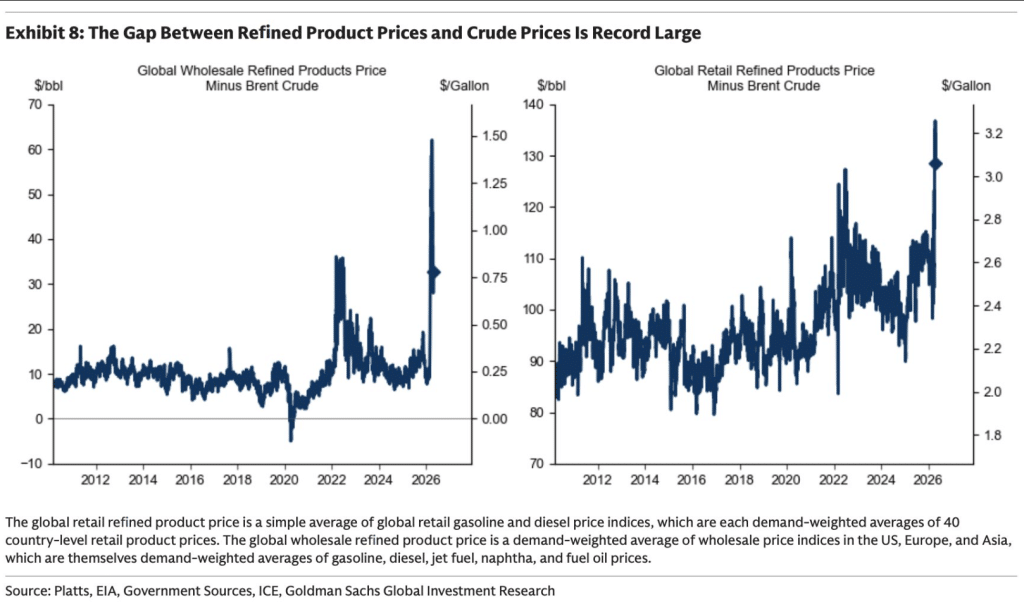

The gap between Brent crude oil prices and refined product prices has reached a record high, as shown in Goldman’s own data. That spread is not an abstract financial metric. It feeds directly into transport costs, manufacturing inputs, and consumer energy bills across every major economy. Goldman also warns that refined product shortages, on top of record inventory draws, mean markets are likely underappreciating the full economic impact of this oil price shock right now.

Goldman specifically identifies South Korea and Japan as petrochemical hubs exposed to feedstock scarcity, with knock-on effects projected for global supply chains in plastics, chemicals, and manufacturing. Goldman’s oil price forecast models point to demand destruction in the Middle East, South Korea, Japan, and Africa, and the bank warns that the shock could force even sharper demand losses if it persists longer than expected.

Goldman Sachs’ conclusion on what this all adds up to is not subtle. This is a systemic global energy shock combining inflationary fuel price pressure, growth drag from demand destruction, supply constraints with rationing risks, and market instability driven by historically low inventories. The oil price trajectory from here depends almost entirely on decisions being made in Tehran and Washington, and right now neither side appears to be in a hurry.

Also Read: US Foreclosures Hit 119K Q1 2026, 6-Year High as Bank Repossessions Surge 45%

Written by Vladimir Popescu

Vladimir Popescu leads editorial coverage at BlockNow, with over 8 years in financial and tech journalism. He previously held editorial leadership roles at Watcher Guru and Windows Report, and has been cited by Forbes for his crypto market coverage.